The mining industry is a fascinating space – not only for the fact that almost everything around us comes from mining but also because of the possibility of striking gold with penny stocks that have the potential to turn into a multi-million dollar mine-producing company. But just as much as there is the possibility of blue sky upside, risk is around every bend even after the mining company has started production, which is why it is crucial to know how to value a mine instead of blindly investing in them.

Many investors and economic enthusiasts are obsessed with gold, but it is hard to break into understanding how one would go about valuing a mine because of a lot of technical jargon. But here’s something outsiders don’t know – every mining company starts out as a cookie cutter of another. For example, how you value a mine is essentially the same, mining executives bounce around companies such that they are all familiar names, and even corporate presentations follow a certain template. Knowing this already is a huge advantage when learning how to value a mining company. In other words, mining is seemingly a mysterious industry, but once you are equipped with the minimal essential knowledge of how to value a mining company, you pretty much know 80% of what you need to know.

We are going over everyone’s favorite: GOLD. Keep reading and you’ll find that it’s pretty simple, and once you learn these step-by-step guide, you might just become addicted to valuing more. Let’s get started.

–A quick interruption: this article is on valuing a mining company. If you’re here for answers on investing in actual gold, this article isn’t it. For that, I would suggest Guide to Investing Gold & Silver. Okay, now that that’s out of the way, let’s really get started. —

(Presumably, you already have a company in mind that you want to value, but if you don’t, the best free resource for finding one amongst a sea of mining companies is 24hgold but you have to pay to view more than 3 searches. Another tool that’s free is simply googling “gold mining feasibility study” and limit search results to the last 6 months.)

Here’s what you need:

- Technical Report

- Valuation Model – (Scroll to the bottom to download gold mine valuation model for free.)

- Company Website

1. Technical Report

Mine Status

Every mine that goes into production has a technical report written by geologists and engineers. This report is called “NI 43-101”. They can be found on the company’s website or in the SEDAR database for a Canadian mining company or on SEC EDGAR for a US mining company. The first page of the technical report will tell you the type of report, which basically means the stage of the mine. These stages are:

- PEA (Preliminary Economic Assessment)

- Pre-Feasibility Study

- Feasibility Study

A PEA is a very early stage report that defines the resources but that is pretty much it. The probability of a mine with a PEA eventually going into production is very low (i.e. just because a mine has a PEA, it does not mean it’s sure to become a mine). The next progression after a PEA is a pre-feasibility study, which has a 10%-30% chance of the mine going into production down the road. It defines the resources with more confidence and discusses the possible economics of the mine (i.e. how much capital costs might go into developing the mine, which is determined by the annual production capacity that makes sense for this particular mine, etc.). The next step after a pre-feasibility study is a feasibility study, which is the most advanced stage of the mine before construction and development begins. It is a more detailed report than the pre-feasibility study with a higher certainty of its assumptions being met. Aside from the majority of the report being a technical assessment, it is essentially a detailed business plan.

By the way, each stage takes years. After a PEA is issued, most likely it will take 2-3 years before a pre-feasibility study and then another 1.5-2 years for a feasibility study. Then anywhere from 1year-never for the permitting process. And finally once you have all the ducks in a row, another 2-3 years for construction and development. In other words, it takes anywhere from 6-10 years before a mine starts producing from the time a PEA is issued. (Note that there is a variance to this time frame depending on many factors. Most notably, a smaller mine in an already mining prolific town where it is easy to get permitting may shave off a couple of years or a big, complicated mine in a politically unstable environment or where there are indigenous protests, may take north of 10 years.)

So, let’s say we settle on a mine that has a feasibility study. As an example, we’ll look at Avnel Gold and its Kalana Gold Project.

What to Extract from a Technical Report

As I said before, there is a lot of technical jargon to understand in mining. And a technical report can be hundreds of pages long. But from my many years of valuing mining companies, you just need to extract the necessary info to value a mine. (Of course, the more of a technical expert you are, the more you can understand the viability of the mine, but most of us aren’t going back to school to get a geology or engineering degree, I don’t think.) So, what to extract from a technical report:

- Mine Start Year

A feasibility is usually optimistic about the permitting process, the length of time for construction and development phase and the pre-production phase. So, I would add 1-2 years to the mine start year that the feasibility study lays out. If the company has already made significant plans to develop the mine after the feasibility study has been issued, you can often find in their annual or quarterly reports or press releases when they expect production to start.

*Note that before full capacity production, the company tests the processing and optimizes the plant. This phase is pre-production and the very first gold produced is called a “gold pour”. We are looking for the year in which “commercial production” starts.

In the Kalana Mine feasibility study, the anticipated commercial production start year is July 2018.

It is highly unlikely for a mine to start producing on time. So, I am going to tack on 1.5 years and say that full capacity commercial production starts in January 2020.

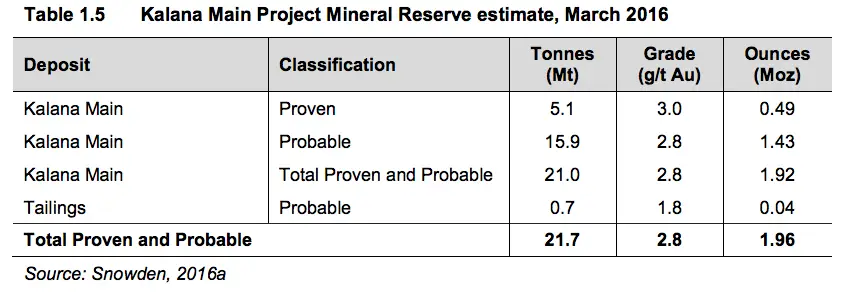

2. Reserves & Resources

By the time a feasibility study is written on a mine, the resources are reported with a high degree of certainty. These are called Proven & Probable Reserves. Each category of reserves or resources tells you the degree of certainty that the stated minerals are indeed there and mineable. If you’re trying to value a mine that only has a PEA, you may only see Inferred Resources. This is kind of a stick your finger in the air and guess how much mineral might be contained in the ore. Well, maybe a little more certain than that. The general rule-of-thumb in converting each category of stated reserves & resources into mineable minerals is:

What this means is, looking at Avnel Gold’s Kalana Mine example, its feasibility study has proven & probable reserves of 1.96 million ounces (or “oz”):

In my valuation model, I’m going to cap the number of ounces produced by the mine at 90% of 1.96 million ounces or 90% of 21.7 million tonnes which is 19.5Mt. Note the grade of 2.8g/t of gold (“Au”) in the table. We’re going to use this number below.

Note that “Tonnes” is the ore (or the actual raw rock) that is mined and processed, “Grade” is how much gold is contained in the ore, and the “Ounces” is the resulting number of gold in ounces. The formula is very simple. It helps us figure out the production rate (discussed in the next section):

*Note: tonnes, not tons. And Troy ounces, not imperial ounces.

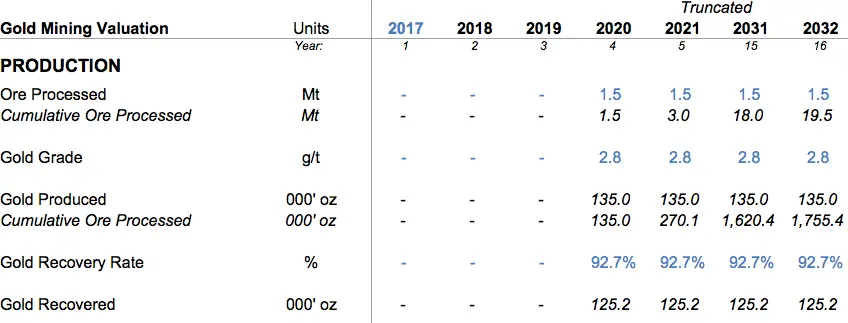

3. Annual Production Run Rate

Under the Economic Analysis section, the feasibility study will lay out the plant throughput. The plant throughput is how much ore (the raw rock) is mined and processed to extract the gold. This is where the “grade” calculation from above is used. In the Kalana Mine feasibility study, the plant throughput rate is 1.5 million tonnes per annum:

Putting together the reserves estimate from above and the annual throughput rate, we model in our valuation 1.5Mtpa per year until we reach a cap of 19.5Mt. That is for 13 years (19.5 / 1.5).

And to convert the 1.5Mt of ore processed each year, using the formula stated above, we multiply it by the grade of 2.8g/t from the reserves table above. That will give us 4.2 million grams. Gold is expressed in troy ounces, so 4.2 million grams is then divided by 31.1035 to result in 135k ounces.

Plopping this into our valuation model with the start year of 2020, this is what it looks like so far:

4. Gold Recovery

Once gold is extracted through the plant at the gold grade, the gold gets further processed to become refined. The Kalana Mine feasibility study states that the Life of Mine (LOM) gold recovery rate is 92.7%, which is extremely optimistic. But for the purpose of this valuation, we will use this number (and because we can always change this assumption later). We simply multiply this to the gold produced to get the refined, recovered gold of 125.2k ounces per year.

5. Operating Costs

The main categories of operating costs are (1) mining, (2) processing, and (3) G&A.

(1) Mining cost consists of all costs associated with excavating the ore (e.g. mine equipment operator cost, fuel cost, maintenance cost, explosives cost, etc.). Expressed as US$ per ounce of gold produced.

(2) Processing cost includes costs associated with the plant, where the ore is processed into gold (e.g. equipment maintenance, plant labor including plant engineers, water treatment, lease, power and utilities, etc.). Expressed as US$ per tonne processed.

(3) G&A cost is comprised of salaries in corporate office, HR, security, environmental costs, land patent tax, etc. Expressed as US$ per ounce of gold produced.

The feasibility study details out the operating costs and also group them which is convenient for the valuation model.

Important to note is that in mining, operating costs are stated as cost per ounce of gold produced. This is for 2 primary reasons: (1) to be able to compare among other gold companies in the industry, and (2) since the gold price is an important economic indicator for the economy in general and for mining specifically, one can easily assess the viability of a mine by netting the gold price by the operating cost, which are both stated in per ounce.

In the Kalana feasibility study, these costs are estimated to be:

– Mining cost: US$380.3/oz

– Processing cost*: $17.68/tonne

– G&A cost: US$74/oz

*Watch out for processing cost expressed as tonne thus calculation is a bit different than the other. See valuation model.

Sometimes, mines have a royalty obligation, which is common when a land owner sells the property to a mining company. The most common type of royalty is Net Smelter Royalty (“NSR”), which is a percentage of recovered gold. At this mine, there is a 3.0% NSR royalty. So we have to account for that.

The government could also collect a royalty – in this case, there is a 0.6% stamp duty on gold sales.

6. Capital Costs (aka Capex)

Are you still with me? We don’t have much to go. Stay with me. It’ll be so worth it. You’ll know how to value any gold mine!

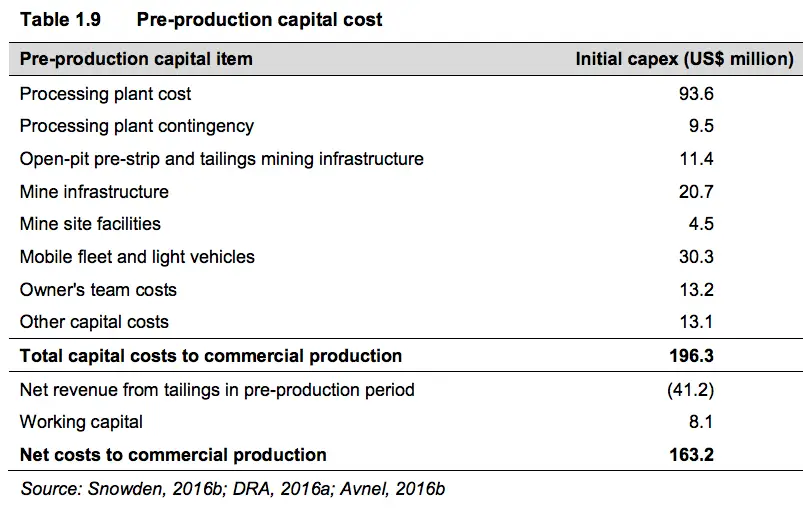

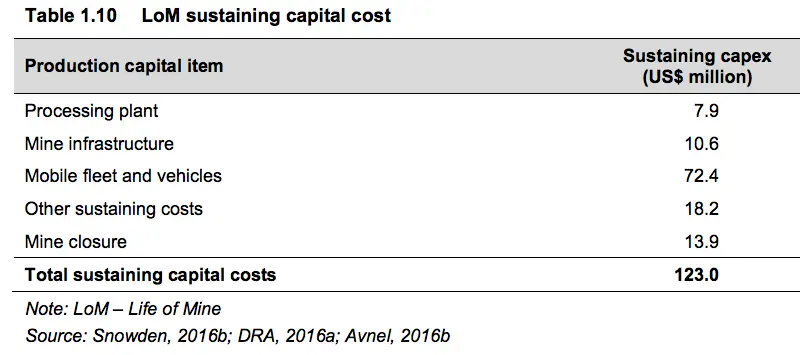

Capital costs are categorized into (1) initial capex and (2) sustaining capex. They are what they sound like. Initial capex consists of construction and development of the mine. All the costs before the plant is producing gold. Sustaining capex is cost associated with maintaining or upgrading all the equipment and assets throughout the life of the mine.

Kalana Mine’s total initial capex (aka pre-production capital cost) is $196.3m.

The total sustaining capex is $123m. Of this total, $13.9m is mine closure cost.

Also provided in the feasibility is a schedule of how the costs are allocated throughout the mine period. However, many companies spread out the initial capex for the sake of the economic valuation. For example, mining fleets are expected to be purchased close to the end of the mine period, which makes no sense but helps the mine be valued higher. So, a rule of thumb is to use the total life-of-mine capex estimates and allocate accordingly:

– Initial capex: 35% in Year -2 (i.e. 2 years before production), 50% in Year -1, and 15% in Year 1. So, if the mine start year assumption is 2020, $196.3m is allocated as such: $68.7m in 2018, $98.2m in 2019, and $29.4m in 2020.

– Sustaining capex: $13.9m mine closure cost will be assumed in the last year, so backing this out, the remaining $109.1m sustaining capex will be allocated among the 13 year mine period, which is $8.4m per year.

This way of calculating is obviously a much simplified version. However, when the discounted cash flow goes out 20+ years, the sustaining capex smooths out to be similar and as for initial capex, having the cost be borne upfront is a more conservative approach so any upside beyond the valuation from this approach is a nice present.

You did it. We have finally reached the end of all the info you need from the technical report to value a gold mine. Out of the ~350 page report, you just need the above 6 data. Not so bad, right?

2. Valuation Model

As you read through the above, we’ve already been going through how to take the info that you extract from the report and put them into the valuation model. So, you should already be somewhat familiar with the flow of the valuation model so far.

A typical microcap mining company (~$100m) has one mine that they are working on (either to bring it to production or they are producing it. But we’re not interested in the already-producing ones because there’s less upside). In other words, they are a single-asset company. As such, the value of the mine minus any liabilities is equal to the value of the company, otherwise known as Net Asset Value (“NAV”).

Because a mine’s economics is a set of cash flows in and out during a defined period of time, the best valuation approach to use is the Discounted Cash Flow (“DCF”), which the valuation model in this example uses. Adding up all of the discounted cash flows, we will derive the Net Present Value (“NPV”).

VALUATION DATE

First, at the top of the model, enter the valuation date that you want to calculate the NPV on. It could be a future date if you want to know what the valuation will be at a future date.

If you are using the model in 2018 or 2019, then you can change the years by changing where “2017” currently is.

If you’ve noticed by now, all of the LIGHT BLUE font means you can change the assumptions and input it directly. Black font cells are formulas so if you enter a value, it’ll mess up the whole model. Only input in the blue font cells.

PRODUCTION

We’ve gone through the inputs and the calculation of gold production above, so we’ll skip this part. One important note is that in a DCF model for a mining company, there is no Terminal Value that catches the cash flows of an infinite period of time beyond a defined time period (for example, 5 years of defined time period and a terminal value for infinite period). The reason is that each mine has a maximum number of contained gold, so it won’t go forever.

GOLD PRICE

If you have access to professional databases like Capital IQ or Bloomberg, then you can look up analyst consensus of gold price forecast, but if you don’t, there are free sites that blog about gold price forecasts. The best place to pull analyst consensus is trustablegold.com. I approach valuations on the conservative side, so I’ve assumed a gold price of $1,300 in the mine start year of 2020 then decreasing to $1,100 until the end of the mine life.

REVENUE AND COSTS

Revenue is simply the recovered gold multiplied by the gold price.

We’ve covered the costs above, both operating costs and capex, so I won’t repeat it here.

The corporate tax rate is different for each mine depending on the country the mine is located in. For this mine, 30% was used. You can quickly look up the corporate tax rate like on KPMG’s table of country tax rates. (Note that there would be allowable tax deductions but these are not incorporated in the model.)

DISCOUNT FACTOR

The higher the risk the mine has in meeting the forecasts, the higher the discount rate. The industry standard is typically in the range of 8% – 12%, with the median being 9%. An example of a 12% discount rate would be for a mine that has political risk, mine development risk, production risk such as uncertainty that the mining method they anticipate will work or if the forecasts in the feasibility study are too ambitious and therefore meeting the forecast is unlikely.

Here, we’ve settled on the industry median of 9%.

NET PRESENT VALUE

We’ve now arrived at the valuation of the mine of $147.4 million. That wasn’t too bad, was it?

Finally, look at the company’s latest balance sheet and add cash and subtract debt to arrive at what the intrinsic value of the market cap is and compare it to the current stock price.

3. Company Website

Now that you know how to value a mine, the next step, which is just as important, is to assess the company qualitatively. This means reading the bios of the Management team and the Board of Directors to see if they have experience in successfully building a mine and using discipline in terms of costs. You can also skim through their press releases to see if they had run into any hiccups in the past related to the mine or any old assets. Or maybe they keep refinancing debt without being able to pay it down. Maybe their accounts payable is growing. Anything fishy or off that catches your eye. Having a keen eye on risk analysis is key.

Interested in valuing copper or lead or nickel or zinc? How to Value a Mining Company, Part II: Base Metals, is posted. Download the base metal valuation model there.

Download Model

Enter your email in the field below and the gold mining valuation model will be sent to your email directly. And you will also be notified of any announcements about this website.

*IMPORTANT EDIT FOR MODEL* A reader brought to my attention a mistake in the model. In line 41, the formula should just be “line 7 * line 37″ in the respective cells. I.e. the formula should not have ” * line 10 / 31.1035″. Also, Cell A54, the label is a typo; it should read “Total Capex”. Hey, we all make mistakes! But on the bright side, this forces you to make changes to the model yourself and actually go through it in detail line by line. Thanks Analyst for catching these and letting me know. Guys, feel free to send him appreciation as a reply to his comment below!

**EDITED** Hey guys, thanks for reading this. I wrote this post and have made the valuation model downloadable for everyone for free. All I ask is that you subscribe and share this site for more industry-specific valuation guides and financial models to download. Thanks very much!

subscribe me please

would like to receive your info on value a mining co

Hi J.S., you can subscribe on the right side of this page. Thanks for your comment!

Would love to download the model.

I found it very very interesting.

Thank you for the post.

Thanks for reading, Bayu! You can insert your email address in the field at the end of the article and it will be delivered to your inbox directly. Cheers!

A very interesting subject. Thank for sharing your knowledge and looking forward to the next one.

Thank you for your feedback, Bailo!

Pingback: Here's how you value any gold project | ValuBit News

Many thanks

Pingback: It’s All About That Base Metal (Free Copper/Lead/Nickel/Zinc Valuation Model Download)

A very interesting article. I found it very useful.

Thank you, Mr. Cohan.

Hi, could you email me the excel valuation model? Thank, I have subscribed but did not receive it.

Hi Kelly, sometimes it takes a few hours (or a day).

Like your methodology.

Plz send me the mining compay valuation spreadsheet

Thanks DaRo. The links aren’t working right now. Send me an email and I can send it to you. Email is: microcap [dot] co [at] gmail [dot] com. Cheers!

Could you please email me the valuation model, the link isn’t working. Thank you in advance!

Thanks Frederick. The links aren’t working right now. Send me an email and I can send it to you. Email is: microcap [dot] co [at] gmail [dot] com. Cheers!

Thank you for this very interesting article. I would like to have a look at the Valuation model but the mailing list seems to have been deactivated. Could you please help me get this model?

Thanks

Thanks Nicolas. The links aren’t working right now. Send me an email and I can send it to you. Email is: microcap [dot] co [at] gmail [dot] com. Cheers!

I am a General Manager of a small mining company in DRCongo and I’d like to have a copy of the model

Hi Geraud,

Thank you for your comment. The link is now fixed. Please enjoy the model and subscribe for more valuation models.

Thanks.

This is a good article for professional geologist and the incoming valuation model will be great as well.

Thanks for sharing.

Hi Christian,

The link is now fixed. I hope you find the model useful. Thank you for your compliment. More valuation models are underway.

Thanks.

Please send Valuation Model

Hi Nicolas,

The link is now fixed. I hope you find the model helpful. More valuation models are underway so hope you subscribe and share with your friends and colleagues.

Thanks.

Great information, please be so kind and email me the free gold mine valuation model.

Thank you

It’s on your way to your inbox!

This is very insightful piece of paper although simplified a lot to make it straightforward. Like it and would you be kind to share the spreadsheet to my gmail inbox? Thank you in advance!

Thanks Sean! Enter your email in the field above at the end of the article and the model will be on its way to your inbox!

Very informative article and model, which will save me a lot of time and energy in evaluating multiple mining companies within a short period of time.

Thanks.

Thanks Alan1!

Please share a actual valuation report if you can?

Thanks Kunal! You can enter your email address in the field above in the Summary section and the model will be sent to your email. Good luck!

Check back in the next month for more!

very interesting article, do you mind sending the sheet at gio_dalpra90@hotmail.it

Thanks Giorgio! I’ve entered your email address in the field above and now it should be coming to your inbox.

Eish …very richly written… I love it please email me the valuation model on how to value a gold mine… Real knowledge

Hi Sipho,

Thank you for your comment! I’m glad you found it helpful. You can download it by entering your email address above in the field. It will send the model directly to your email. Cheers.

Hi,

Many thanks for the valuation model.

I just wanted to check on the formula for Processing Costs. You’ve used the formula =H$7*H37*H10/31.1035

Should it just be (Ore Processed) * (Processing Cost Per Tonne) = $26.55mln rather than $2.4mln?

Also, should the Capex line with Initial, Sustaining and reclamation total to Total Capex Costs rather than Total Operating Costs?

All help is much appreciated.

Hi Analyst,

GREAT catch. I am embarrassed that I made that error! I’ve added an edited comment for readers. And yes, it should be Total Capex Costs, not Total Operating Costs. I’m impressed that you went through the model in detail and caught these. If you’re interested in writing about mining valuation for this site, send me an email (contact info under disclaimer page). Thanks for your interest on this site and hopefully found it helpful. Cheers.

Today (December 25, 2020), I received the valuation medal, yet there was no editing comment regarding H41 and A54. When H41 is changed from 2.4 to 26.5, NPV will drop to 45.1. Do you agree?

Hi,

I have a question regarding the valuation (im new to this, so it might be a stupid question). I get that in general the juniorcompany NAV equals to Project NPV + net cash. But in the case of a junior miner you probably need to calculate the dilution (or future debt) to finance the Project CAPEX since very few juniors got the cash.

If so, should the valuation formula be Project NPV + Net cash – dilution (which would equal to CAPEX) ?

Thank you

Pelle Jons

Sorry about the late reply! If the debt hasn’t occurred yet, it’s probably best not to include in the calculation.

Thanks a lot for this model. I was wondering why CapEx is subtracted prior to the tax expenses. Is CapEx for gold miners tax deductible?

Thanks!

Yes, capex should be calculated through a depreciation table, and it should be tax deductible. Thanks for your comment!

This is very informative. I have watched some YouTube videoes and this is the best I have found. For someone who is looking for something simple and yet effective, this was a great article. But, is there an excel template that you could share or sell?

Very nice page explaining this stuff, will be helpful. Just downloaded the model in excel but it indicates it’s corrupted. Any way to have this fixed?

Thanks for your comment! Hmm, I’m not sure why it says corrupted. It seems to work fine for other downloaders. Have you checked that it’s compatible with your Excel?

The link for Gold model is not working.

Please can you send it to my mail?

Hi Paul, if you enter your email above, the model will be sent to your email directly.

Thanks for the strong primer!

Thank you, Harold!

Very useful and detailed information

Thanks for sharing

Thanks J.!

Try the model

Thanks Eddie, looks like there was an issue. Let me know if the email with the attachment went through to you.

Hello, great valuation model, thank you.

How do we convert the US$/oz to US$/tonne mined, milled or processed?

E.g. one miner I am looking at reports AUD 13.8 / tonne processed, no per oz cost. How can i get this to the per oz figure?

Thanks

Hi Johan, I explain how to convert tonnes milled to ounces of gold produced (Ctrl + F “31.1035” to jump to that section). To go from oz to tonne, you can just reverse the calculation but you will always need grade of the gold in oz. Your question of US$/oz to US$/tonne is the same – you will need the grade to calculate approximately how much the US$/tonne mine/milled is. It could be that the company you’re looking at might not be advanced enough (and still a junior explorer) and thus might not have the grade. Hope that helps!

I cant seem to access the model

Thanks for notifying me. There was a back-end issue, but now it’s fixed and you should be able to get it delivered to your email. Cheers.

Thank You! Great article and thanks for the resources!

Glad it worked! Thanks for reading and happy to share!

Hi MC,

I would like to get the valuation model too.

Thank you for sharing.

JG

It should now be up and running and on your way to your email! If not, then there now should be a field for your email address.

Very informative, thank you for sharing your knowledge! I would love to see the valuation model if possible.

Thanks for reading, Jaromy! The glitch is fixed for now, so the model should be on your way to yo email.

I would be grateful for the template of a DCF for mining and exploration projects

Thank you

It should be on its way to your inbox!

Nice Article.

Thanks very much!

I would like to consult with you regarding mineral(gold) rights valuation for an Estate Tax Return.

Can you please contact me?

Hi James, thanks for your comment. I’m afraid I don’t do consultations, but if there’s a reader who’d like to contact James, please leave a comment here to be connected. Thanks for reading!

I would like to get the valuation model too.

Thank you for sharing.

Should be on the way to your email!

Hi, can I get the model somehow?

Should be in your inbox now!

I really enjoyed your article. Could I get a copy of the model please?

Thanks

Thanks Ian! Sent!

send me a copy please

Sent!

Hi, Would you please send me the valuation model spreadsheet. I already emailed you in this regard. My email is: pr_raheem@hotmail.com

Thanks in advance,

Should be in your inbox from microcap.co!

Hi,

Could you please send me the valuation model spreadsheet? I’ve already subscribed to the website but I haven’t received anything yet.

Thanks,

Bib

Sorry for the late reply, Bib. Did you put your email address in the field at the end of the article? It should be working now but let me know if it still doesn’t work!

Please send me the spreadsheet valuation model? Cheers

Sent!

Any way I could be sent the model?

Sent!

Hi,

Is it possible to share this model. I have used this methodology to value Evolution Mining.

Thanks,

Vi

Sent!

Looks interesting, I wouldn’t mind having a look but the link didn’t seem to work. Can you sent to my email?

Hi Blee, thanks for your comment. You can put your email address in the field at the bottom of the post and the model should be sent to you directly!

Great stuff! would you please share model with me? Thank so much!

Thanks very much! You can put your email address above the comments at the end of the article and it will be emailed to you directly. Cheers!

This is very helpful! Thank you for sharing 🙂

Thank you, Althea! I’m happy it was helpful!

Thank you very much for sharing your knowledge. This was very helpful!

Thanks, Rodrigo! Really appreciate your comment 🙂

Thank you for a really informative article. It was just what I needed. Wishing you every success.

I’m happy to hear that! Thank you for commenting!

Hi analyst,

I have just come across this site, is it still possible to subscribe and obtain the gold mine valuation model now? The subscribe section of the page does not seem to be working anymore.

Thank you.

Ah, the automatic mailing system keeps glitching. Thanks for letting me know; it should be in your inbox now!

Hey Mate, This was super helpful!!

Is there any chance you could send a copy of the model to kempie98@gmail.com?

Thank you!

Looks like I have to fix this glitch. It should be on the way to your inbox, Joshua!

Hi

Please send me the valuation model.

Thanks

Gillian

Sent to your inbox!

Excellent article, thanks for posting!

Thanks Billy! The file has been sent to your inbox if you were looking for it!

Very informative content. I’m doing a thesis by doing a comparative study of development of new gold projects in Select African & European countries. I need to Evaluate the Competitiveness of each country’s fiscal policy. Definitely I will use this model. Do you have some projects you have done using the model which you can send me or any extra material which can assist my research. My email is godfreymwelelu@yahoo.com

I’ve already subscribed. Thanks in advance

Thanks for your comment, Godfrey, and I’m happy to hear this is helpful! Unfortunately, all my financial modeling were at my previous employer’s and I am not able to share them due to confidentiality. Good luck with your thesis!

Looking forward to the read

Thanks!