The apparel industry in 2024 reflects a rapidly evolving landscape with significant changes from past trends.

In 2024, sustainability has transitioned from a niche consumer preference to a financial and regulatory necessity.

Unlike previous years, where sustainability was predominantly driven by brand image, this year has seen stricter environmental regulations in the European Union and California mandating supply chain transparency and emissions reporting.

This shift has pressured brands such as Levi Strauss and Adidas to accelerate investments in circular fashion, such as resale and repair programs.

Globally, the apparel sector has witnessed heightened collaboration between brands and governments to meet carbon neutrality goals, a sharp departure from the largely voluntary sustainability initiatives of earlier years.

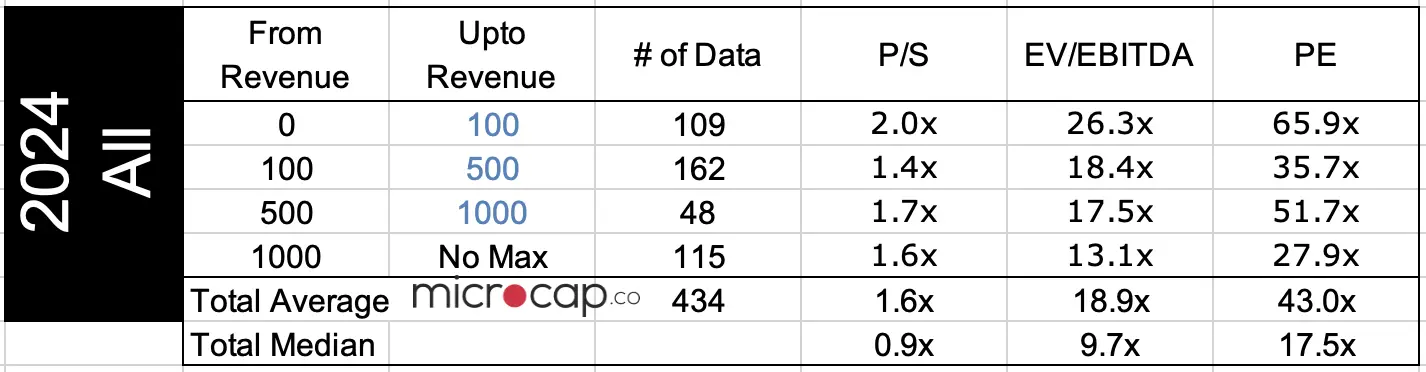

Apparel Industry Valuation Multiples

We saw slight changes for revenue multiples and EBITDA multiples for 2024 and a bigger change in the PE ratio.

Out of 434 companies, the average revenue multiple is 1.6x and the median revenue multiple is 0.9x.

The average EV/EBITDA multiple is 18.9x and the median EV/EBITDA multiple is 9.7x.

The average PE multiple is 43.0x and the median PE multiple is 17.5x.

All the valuation multiples increased compared to 2023.

What Affected Apparel Companies Valuation in 2024?

The differences in valuation metrics for public apparel companies between 2023 and 2024 reflect the industry’s evolving dynamics.

Here’s a breakdown of how industry trends may have influenced these changes:

Price-to-Sales Ratio (0.7x in 2023 to 0.9x in 2024)

The increase in the price-to-sales (P/S) ratio suggests that investors are valuing revenue more highly in 2024 than they did in 2023. Several factors could explain this:

- Many apparel companies have shifted towards higher-margin premium product lines (e.g., Athleisure 2.0). This has increased average revenue per unit, boosting overall sales figures.

- Growth in direct-to-consumer sales, which tend to have higher margins, may have contributed to improved revenue performance.

- In 2024, consumers displayed stronger-than-expected spending habits on discretionary items like apparel such as in the U.S. and Europe.

EV/EBITDA Ratio (8.6x in 2023 to 9.7x in 2024)

The rise in the enterprise value to EBITDA ratio points to increased investor confidence in the industry’s profitability and cash flow generation. Key drivers may include:

- Improved EBITDA margins from increased operational efficiency.

- A resurgence of physical stores was seen in 2024. This may have contributed to higher EBITDA margins.

- More predictable inventory management compared to 2023 as supply chain has made a comeback to steady levels since the pandemic.

P/E Ratio (10.9x in 2023 to 17.5x in 2024)

The substantial jump in the price-to-earnings (P/E) ratio indicates that investors are willing to pay more for each dollar of earnings, reflecting stronger growth expectations. This could be attributed to:

- A shift towards premium brands that have higher-margin products, such as luxury athleisure and sustainable apparel.

- High M&A activity, particularly among high profile companies may have created synergies that increased profitability with heavier weighting.

- 2023 itself may have been a weak base year as a comparison since it was still a year following the pandemic recovery.

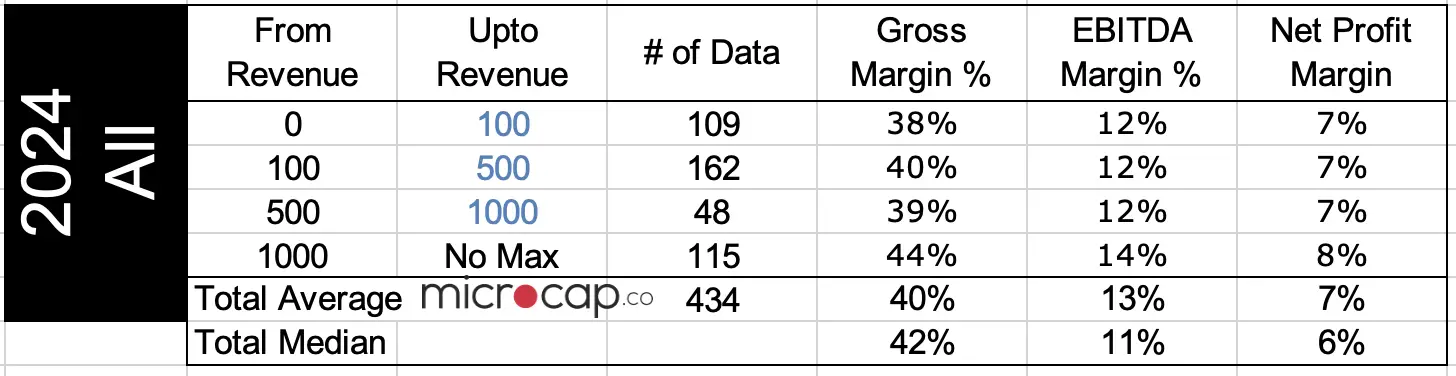

Apparel Companies Margins

The gross margin, EBITDA margin, and net profit margin all increased slightly from 2023.

The explanations for these higher margins may be explained by higher operational efficiency, improved inventory management, more prominence of premium brand companies that have higher profit margins.

Expectations for Future Trends in 2025?

- Sustainability and Circular Fashion Models: The industry is expected to face increased pressure to adopt sustainable practices, including recycling and circular economy principles, to meet consumer demand and regulatory requirements. Source: McKinsey

- Technological Advancements and AI Integration: The adoption of AI and other technologies is anticipated to enhance personalization, inventory management, and operational efficiency, potentially impacting profitability and valuations. Source: FashionUnited

- Geopolitical Supply Chain Shifts: Ongoing geopolitical tensions may drive companies to diversify their manufacturing bases, affecting operational costs and supply chain stability. Source: WSJ

- Emerging Market Growth: Regions like India and Southeast Asia are projected to experience significant market growth, offering new opportunities for expansion and revenue diversification. Source: GM Insights

- Luxury Market Dynamics: The luxury segment may encounter challenges due to shifting consumer behaviors and economic factors, influencing its growth trajectory. Source: Vogue

Download 2024 Dataset

To download the 434 companies data set in this analysis, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly. In some cases, it takes a few hours or a day to receive the email with the data set.