Manufacturing is a very broad industry. Manufacturing could mean anything from food manufacturing to heavy machinery and equipment. What I’m interested in the most is manufacturing in the general industrial category that can be loosely applied to any sub industry of manufacturing. So, I analyzed the EBITDA multiples for manufacturing companies in the general industrial segment, electronics, and machinery tools.

I first screened for those sub industries. Then, I removed companies that had negative earnings or negative EBITDA. And finally, I removed outliers as they were causing the sample set to be pulled in extremes. Here is what I learned. But first, let me take you through the rationale for using EBITDA multiples to value manufacturing companies.

Why Use EBITDA Multiples For Valuing Manufacturing Companies

Arguably, the most important things for a manufacturing company are:

- Assets – particularly, capital assets such as machinery and equipment.

- Efficiency and process – is the operation running at optimized efficiency? Because this affects margins and therefore profitability.

- Liquidity – how much debt is on the balance sheet? Manufacturing companies tend to hold a lot of debt, because they are capital intensive and need equipment financing to set up their plant. So, the question here is will their cash flow meet all the debt covenants? If not, is there a risk of defaulting on their loans?

So, when I was evaluating a paint manufacturing company and a household appliance manufacturing company, the above key points were what I started with before digging into the company’s data. So, all these were fine when I was analyzing the financial health of the company on a standalone basis.

However, when I wanted to analyze the company based on how they were doing compared to their competitors, it was hard to rely on the above points to make a comparison.

In other words, manufacturing companies are so specific in what they do in terms of how they run the operation and how much capital asset is required, that I had to rely on a different measure to determine whether the company was undervalued or overvalued in terms of the purchase price.

In my opinion, EBITDA (see definition here) was the most comparable measure for manufacturing companies in general, for the following reasons:

- CAPEX will vary largely depending on how capital intensive the manufacturing company is in that industry, so we want to look at a profitability figure above CAPEX, which EBITDA is.

- One of the important factors that determine whether a manufacturing company has the financial and operational strength is their operation efficiency, which is their operating cost management. We want to capture the operating cost and EBITDA is a measure that captures that.

- Looking at EBITDA margin also gives us a look into the company’s efficiency and profitability compared to their peers.

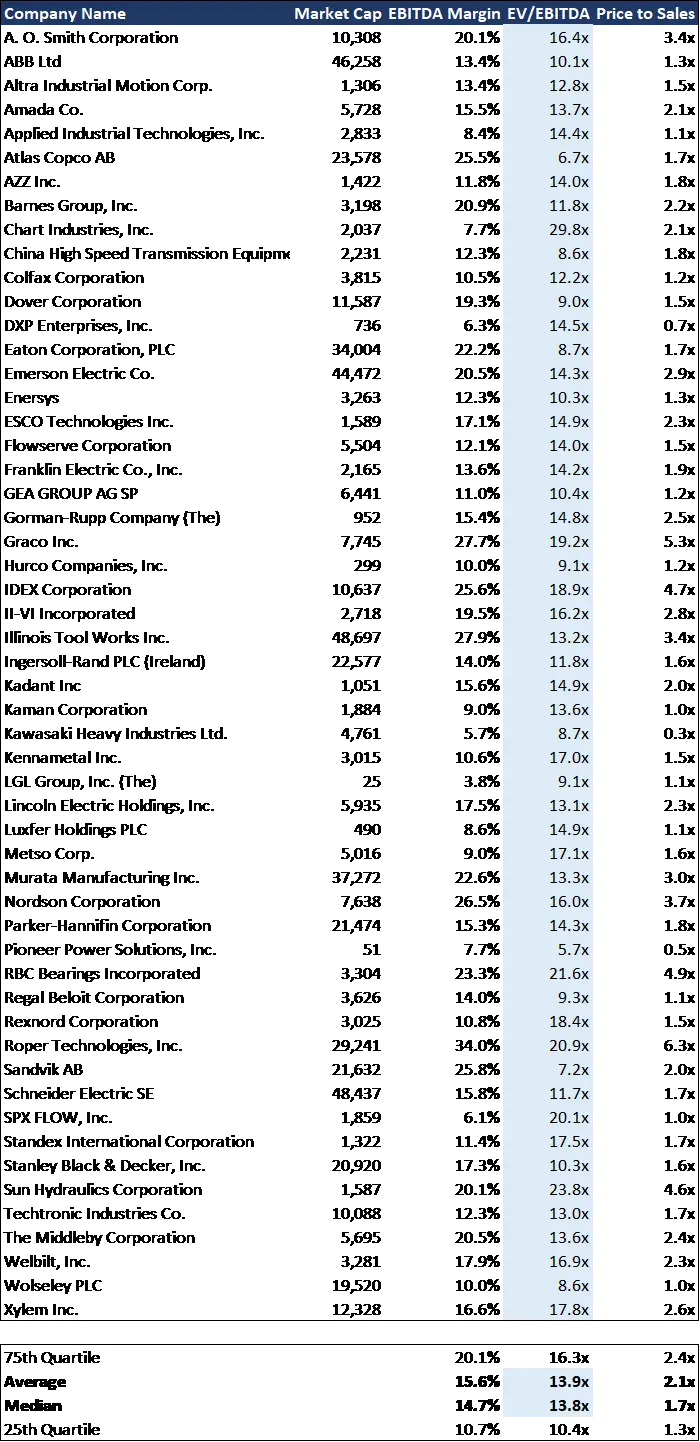

Average EBITDA Multiples Using 50+ Manufacturing Companies’ Data

Pulling data from 50+ manufacturing companies in the general industrial segment of manufacturing, the average EV/EBITDA multiple was ~14.0x. Here’s the breakdown of the data and how I got to 14.0x.

But first, some interesting key observations:

- The higher the EBITDA margin, the higher the EV/EBITDA multiple valuation.

- There isn’t a linear relationship in the size of the company and the EV/EBITDA multiple, but the small set of micro cap companies have a EV/EBITDA multiples below the average.

- Average EV/EBITDA multiple is 13.9x and the median EV/EBITDA multiple is 13.8x.

- Average price-to-sales multiple is 2.1x and the median price-to-sales multiple is 1.7x.

- The more technical, precise and skilled the manufacturing industry, the higher the EV/EBITDA multiple. For example, medical equipment manufacturing companies tended to have an EV/EBITDA range higher than the average general industrial. And simple silicon or plastic manufacturing process had an average EV/EbITDA multiple below the average of the general industrial. (Note: the data set shown here doesn’t include companies other than general industrial but my research included those segments).

How To Use Valuation Multiples To Value a Company

For those who are not familiar with using valuation multiples to value companies or those who are but need a refresher, I wrote posts detailing exactly how you can do that.

Hopefully you can use them as helpful guides. Click on the link below to go to the post.

- How to value a company based on revenue

- How to value a company based on EBITDA

- How to value a company based on earnings

- How to find your own valuation multiples

- Other posts on how to value a company

How To Use The Average EBITDA Multiple

Okay, great. So the data above shows us that the average and median EV/EBITDA for manufacturing companies is about 14.0x. What do we do with this data? Principally, you can use this number to value the subject manufacturing company:

1. If the subject manufacturing company is private and you are interested in calculating the approximate purchase price of the company, you can start with multiplying 14.0x to the EBITDA of the company. Then you subtract debt and add cash to get to the equity value.

For example, say you’re currently contemplating the acquisition of a small semiconductor manufacturing company in California. And after going through their historical financial statements, the last twelve months EBITDA is $2.5 million. Then you multiply $2.5 million by 14.0x to get an enterprise value of $35 million.

You’ll have to make a few more adjustments to derive the purchase price of the company. Since you’d have to assume the debt on the balance sheet, you would subtract the EV by the debt. If debt for this hypothetical company is $5 million, then you’d subtract $35 million by $5 million and arrive at $30 million.

Then, if there’s excess cash sitting in the bank, you can either add that to the $30 million or the seller of the company can keep that cash and you wouldn’t make any adjustments to the $30 million.

2. Another way you can use the EV/EBITDA multiple is to gauge whether a public manufacturing company you are contemplating buying the stock of is overvalued, fairly valued or undervalued. Pull up the financial statements of the public company and determine the most recent twelve months’ EBITDA. Find the company’s enterprise value (which is market cap + debt – cash). Divide the EV by the EBITDA. If this multiple is below 14.0x, then the stock is undervalued. If the multiple is above 14.0x, then the stock is overvalued. If the multiple is around 14.0x, then the stock is fairly valued. If the company’s size is micro cap (i.e. market cap is below $300 million), you’d want to discount its multiple so if it’s say 10.0x, then it is not necessary undervalued.

Note that the above is a very simplified hypothetical example and there are many factors that determine a company’s valuation. This post is an illustration and an example using a dataset of 50+ manufacturing companies in the general industrial segment of what their EBITDA multiples are.

A rough estimate and a rule of thumb is always a great starting point. If you need more info, keep digging as you never know what surprises the company may hold in store. If any comments or questions, leave me a comment below!