How To Value A Pre-Revenue Startup

Before we start on valuing a pre-revenue startup, perhaps you’re looking for something else?

- If a startup has had at least a few years of revenue, then you can use the startup valuation multiples to value the company.

- If the company you’re valuing is NOT a startup but it has no revenue, you can read about that here.

If you want to value a startup and it is pre-revenue, then stay here as we’ll go through the common methods to value a pre-revenue startup below.

These methods are not perfect, so in most cases, several different valuation methods are used together to arrive at a reasonable valuation.

Generally, investors put a higher valuation on pre-revenue startups with the following characteristics:

- Has traction; i.e. they started not too long ago and they’re already starting to gain traction with new customers without paying a high cost for customer acquisition

- An experienced and diverse team that shows commitment and dedication (if they have track record of successful startups, then a higher premium will be placed on the valuation)

- If the startup has early proof of its vision with a minimum viable product (MVPs)

- Patented technology in a hot space

Scorecard Method

The Scorecard method is what it sounds like. A list of characteristics is scored for the startup and compared to the valuation of a similar startup that has recently been valued.

For example, let’s say a Yellow Tech company is a startup that uses machine learning to detect credit card fraud, and it was valued last year at $10 million.

Now, let’s say we have another startup that we want to value called Auburn Tech company and the company does something similar, which is to use machine learning to detect fraud or other threats.

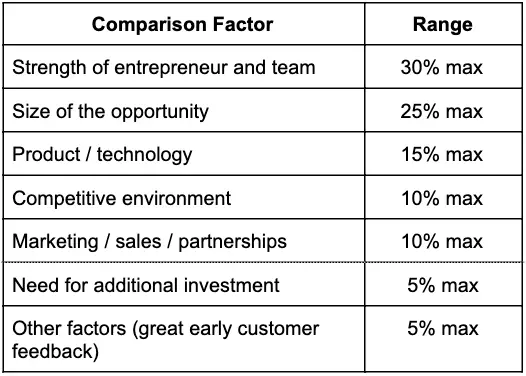

Step 1) The starting scorecard looks like this (source: You can read more about the scorecard valuation method here by the inventor Bill Payne):

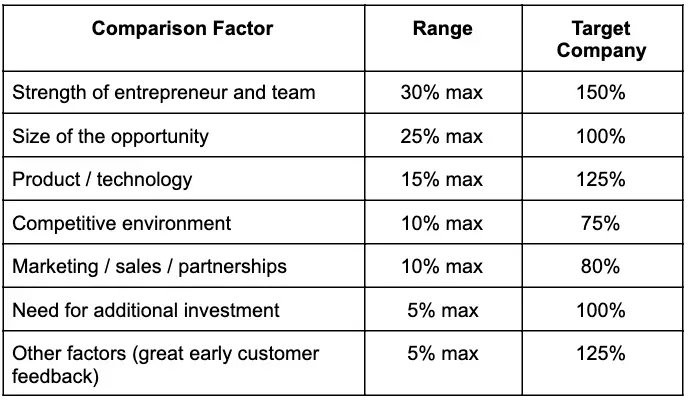

Step 2) Now you look at each characteristic for Auburn Tech, the startup you want to value, and give it a score out of 100% (You can go above 100%).

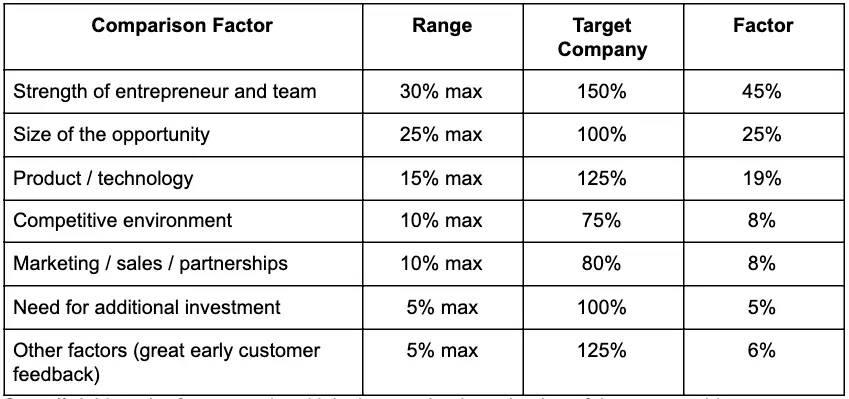

Step 3) You multiply the given range for each characteristic by the score you gave for the target company to get the “Factor” column:

Step 4) Add up the factors and multiply the sum by the valuation of the comparable startup.

In this case, the sum of the factors is 116%.

The valuation of the comparable startup, Yellow Tech, was $10 million.

So, when you multiply 116% to $10 million, the valuation of Auburn Tech is $11.6 million.

The scorecard valuation method is not perfect, because as you can see, there is a lot of subjectivity. And, it’s hard to come by exactly the same comparable startup that has a valuation which you can use as the comparable company.

But, without any revenue, this is one method to value the pre-revenue startup.

Berkus Method

The Berkus Method is another valuation method named after the inventor. It was developed by Dave Berkus, who is an angel investor. It was created in the 90s and he updated it in 2016, which you can read about here.

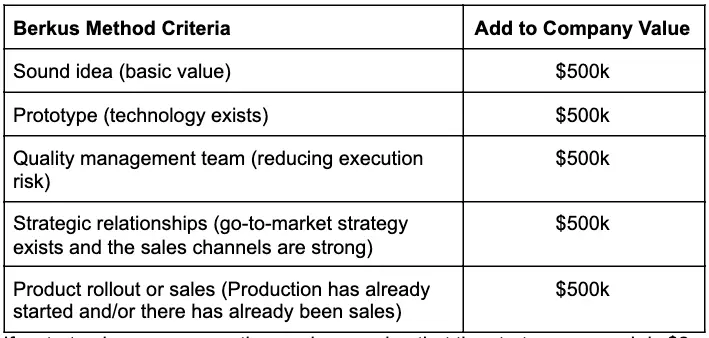

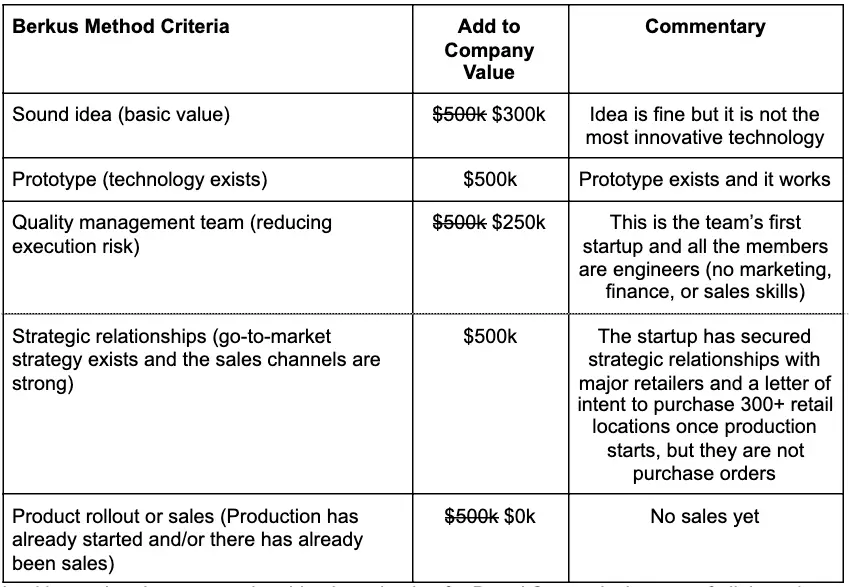

The Berkus Method is quite simple. It assigns up to a max of $500,000 per criteria, which can give a maximum of $2.5 million in valuation.

The criteria are:

If a startup is pre-revenue, the maximum value that the startup can reach is $2 million since the last criteria is attributed to if the startup has already produced and started selling.

For example, let’s say Bread Startup has created a prototype that automates the sourdough bread making process. An example criteria for this startup can be:

Looking at the above example table, the valuation for Bread Startup is the sum of all the values in each category, which is $1.55 million as of today.

Note that the category in the Berkus Method can be customized to a specific industry.

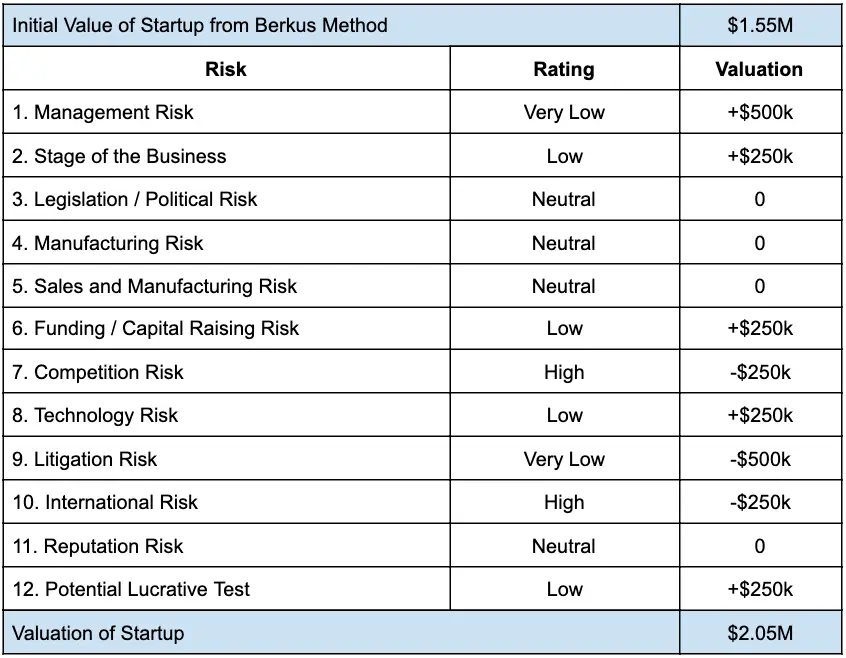

Risk Factor Method

The Risk Factor method is like an extension of the Berkus Method. You apply the same method of + / – up to $500,000 based on the characteristic.

The Risk Factor method has more characteristics to either add or take away value from the overall valuation.

The Risk Factor Summation table looks like this:

You can use a different rating system and customize the risks for the industry.

If you use the “very low to very high” rating system, you can plus $500k if the risk is very low, you can plus $250k for risk that is just low, 0 for neutral, and you can minus $500k if the risk is very high, or minus $250k if the risk is high.

Or you can use the -2 to +2 rating system, where you minus $500k for -2 and plus $500k for +2.

The point is, whatever rating system you use, this method was designed so that you plus or minus up to $500k for each risk evaluation criteria.

Extending the example from the Berkus Method where we got a valuation of $1.55 million, let’s see what happens when we rate the startup using the Risk Factor Summation method:

For each risk criteria, record a rationale that justifies the rating you gave.

Venture Capital Method

The Venture Capital Method (or VC Method) looks at future revenue that hasn’t been proven yet, so this method is a bit precarious.

If a startup is pre-revenue to begin with, it’s really hard to predict what the revenue will be in the future.

But this method was invented by a professor at Harvard Business School in 1987 named Bill Sahlman, and it is a popular method that investors still use. You can read more about Professor Sahlman’s publication here.

How it works:

Step 1) Project future revenue for the next 10 years.

Step 2) Multiply that revenue by the projected profit margin.

Step 3) Multiply the projected profit earned over the next 10 years by the industry P/E ratio. This gets you the “post-revenue” valuation.

Step 4) Take the post-revenue valuation and divide it by the return on investment (ROI) that the investor is expecting. Then, subtract that by the investment amount to get the pre-revenue valuation.

For example, let’s say a wearable tech startup that is currently pre-revenue projects that in the next 10 years, they will be able to generate $5 million per year. And after doing a cost analysis, their estimated profit margin is 20%.

First, multiply the projected revenue by the profit margin: $5 million x 10 years x 20% = $10 million.

The industry P/E ratio is 10x. The post-revenue valuation is $10 million x 10 = $100 million.

An investor is investing $3 million and expects a return on their investment by a multiple of 20.

The pre-revenue valuation is $100 million / 20 – $3 million = $2 million.

Note that VC firms and investors will modify this method quite a bit to their investment standards and philosophy.

Here is a great free resource created by Sam Kwok, where you can download a copy of the Venture Capital Method templates and value the startup yourself using the template.

Summary

When valuing a startup that is pre-revenue, the above common methods help you look at each characteristic that investors have deemed as the most important characteristics that help predict success or failure of a startup.

But of course, they are all assumptions today and there are many factors at play that actually make or break a startup.

As a final note, make sure that you not only use one method in isolation but use several methods to estimate a reasonable value of the startup.

Whether the company has revenue or not, it is always a good idea to use several valuation methods and triangulate a reasonable value. It allows you to sense-check the valuation from one method with another.

And finally, the last thing I want to say is that having worked in the business of valuing companies and building business cases for over a decade, valuing a company using standard methods in a vacuum is like going to a store and being blind folded when buying when you need.

You have to consider other qualitative factors and a lot of that comes from experience.

A good place to start if you don’t have professional experience, is the book, Venture Capital Mindset by Renata George.

The book is geared towards an aspiring venture capitalist, but it provides a great framework for how to evaluate startups at a high level and is really useful for investors, entrepreneurs, and financial analysts.