Manhattan Bridge Capital (NASDAQ:LOAN)

The first company I am adding to the official microcap.co portfolio is Manhattan Bridge Capital (NASDAQ:LOAN). I have to say that at first glance of their website, I was completely put off. The website looks like a school project. But it passed my initial sniff test, so I decided to look past the unprofessional looking website.

From learning more about the company, the aesthetics match my analysis of the company. It’s a small group, really a one-man band. The business is lean and very simple – a hard money lender (i.e. short-term lending to real estate development investors with real estate as collateral) in the New York metropolitan area. There aren’t layers of complex operations but rather, what you see is what you get which is good because there are only few factors that could go wrong to drive the business into the ground, but on the same token, there isn’t blue sky upside.

So, is Manhattan Bridge Capital stock worth it?

First, The Business

The company was founded by Assaf Ran in his basement in Queens in 1989. Ran started a Jewish yellow pages publication company known as DAG Media. In 2007, the company started a lending operation, allocating $5 million lending to businesses. In 2008, the company reported that its lending operation was the most profitable, so Ran changed the name from DAG Media to Manhattan Bridge Capital and listed on NASDAQ under the symbol LOAN. And so the story really begins in 2008, ironically, a great year to really launch a lending business.

Despite many challenges MBC went through over the years, I appreciate that Ran is a scrappy entrepreneur who wouldn’t let his business fall by the wayside. When the Jewish yellowpages business wasn’t performing as well as it used to, Ran started lending to businesses, and when he saw that this was a more profitable business, Ran pivoted the company completely to lending in the niche of short-term lending to real estate investors in metropolitan New York.

The Business Model

Manhattan Bridge Capital lends typically in the range of $300,000 – $600,000 for 12 months (often with extensions) to real estate investors developing residential or commercial buildings in the New York metropolitan area.

Every loan is secured with a first lien on the building and a personal guarantee from the borrower, which may or may not include the borrower’s equity interest in the real estate project. The company apparently has as rigorous due diligence as the big banks but the approval of the loan is much much quicker at 3 to 10 business days. The loan-to-value is a conservative 75% and 80% for construction costs.

The loan portfolio consists of 3 types:

- Purchase, fix and flip

- Small/New Construction Projects single and multi-units

- Income Producing Properties

The loans are currently charged at 11% – 14% interest rate. Currently they have ~120 loans outstanding. Since 2007 when they started lending to real estate investors, the company has closed ~620 loans and *knock on wood* there has not been one default on the loans.

How I Analyzed the Business

As a microcap analyst, analyzing the financials of the business is not as important. The company might be at the cusp of an explosive growth. The business might not be breaking even yet but have been working on an innovative idea that could disrupt the industry.

More important in my experience of microcap companies are looking at the capability of Management, the idea/product – can it scale and is it innovative, and is the business’s operation robust or are they amateurs without a proper system in place?

This is one of the reasons I truly enjoy analyzing and investing in microcap stocks. It’s a more qualitative process more than anything else. You can approach looking at a microcap stock in any number of different ways and there is no right or wrong. I admire analysts’ work but it gets pretty boring for me looking at blue chip stock analyst reports that follow a certain template. Picking the best microcap stocks involves more about really understanding the underlying operations of the business, not about hype or what the mob thinks. Don’t get me wrong – if you don’t have a disciplined investing philosophy, it could be a disaster.

Anyway, the reason why I like this company particularly is because the business model is simple, which means there isn’t a myriad of factors that could screw up the business. On the flip side, if one of those few factors go wrong, it can be detrimental to the business.

This is how I valued Manhattan Bridge Capital, starting with the most critical questions in Tier 1.

Tier 1 Analysis Questions:

1. Are they earning a spread on interest earned and the funding cost?

They’re earning 11% – 14% interest on 1 year short-term loans. Plus, if the borrower can’t pay the principal in a year when it’s due, the company will often extend the loan at a premium.

The cost of equity – which is critical for MBC since they’ve been raising equity financing every year – is probably 6% – 8%. The company’s cost of debt is 6%.

So, the company’s spread on the interest earned and their cost of capital is 3% – 8%. If the company’s operating cost; i.e. CEO compensation, staff salary, office cost, is reasonable, then that’s a chunky spread. Since 2014, the company has been registered as a REIT, so 90% of their earnings is passed through to the investors, which means there’s more meat on the bones for the investors because there’s no corporation tax and 90% has to be paid as dividends.

2. Reasonable operating expense?

So that brings me to the next question of whether the operating expense is reasonable. 2017 G&A was $1.227m which is a 22% increase from 2016 G&A of $1.006m. Their annual report says that the increase is “primarily attributable to bonuses to officers and increases in payroll, board compensation, travel and meal expenses.” That is a pretty hefty operating cost considering the company consists of 2 officers, 3 operations personnel and 3 board members excluding the CEO. But the company’s net income and dividends paid did increase by the same amount of $600,000, so the company isn’t cutting their bonus check from what the investors “earned”. This indicates to me that the business is still a “family” business run very close to heart of the CEO so he will take what he thinks he deserves first and foremost but more importantly, he won’t take more than what is on the table to the detriment of the investors. A good sign of a CEO’s character.

3. Do they ensure creditworthiness of their clients?

The company states that their due diligence process is as rigorous as the banks but their approval time is much much quicker at 3 to 10 business days. In their annual report, they discuss the due diligence process as:

“In terms of the property, we require an assessment report and evaluation. We also order title, lien and judgment searches. In most cases, we will also make an on-site visit to evaluate not only the property but the neighborhood in which it is located. Finally, we analyze and assess financial and operational data provided by the borrower relating to its operation and maintenance of the property. In terms of the borrower and its principals, we usually obtain third party credit reports from one of the major credit reporting services as well as personal financial information provided by the borrower and its principals. We analyze all this information carefully prior to making a final determination. Ultimately, our decision is based on our conclusions regarding the value of the property, which takes into account factors such as the neighborhood in which the property is located, the current use and potential alternative use of the property, current and potential net income from the property, the local market, sales information of comparable properties, existing zoning regulations, the creditworthiness of the borrower and its principles and their experience in real estate ownership, construction, development and management. In conducting our due diligence we rely, in part, on third party professionals and experts including appraisers, engineers, title insurers and attorneys. Before a loan commitment is issued, the loan must be reviewed and approved by our Chief Executive Officer. Our loan commitments are generally issued subject to receipt by us of title documentation and title report, in a form satisfactory to us, for the underlying property. We require a personal guarantee from the principal or principals of the borrower.”

4. Does Management have a track record of success?

Assaf Ran, the CEO and founder of the company started the business in 1989 as a Jewish yellowpages business. Slowly and steadily, he grew the business. He saw an opportunity to lend to small businesses and when the lending arm became more profitable and the yellowpages was declining as expected from switch to technology, he made the decision to pivot the company completely to a real estate lending business. He didn’t start out as a real estate lender but being in this business since 2007 has earned him the stripes.

Tier 2 Analysis Questions:

5. Is their revenue generation defensible?

Here what I’m looking for is where they originate their deals from. How much of their revenue is recurring and is there a risk that the number of borrower approaching them declines? According to their 10K, the company relies “on our relationships with existing and former borrowers, real estate investors, real estate brokers, loan initiators, and mortgage brokers to originate loans. Many of our borrowers are “repeat customers.””

Great news as long as the New York metropolitan market continues to rise. But if there comes a day when the market is no longer attractive or the market is saturated and the real estate demand (whether residential or commercial) starts to decline, they’ll be in trouble. I don’t see that happening in the short term or medium term, for that matter.

6. Does the company have a positive, increasing cash flow?

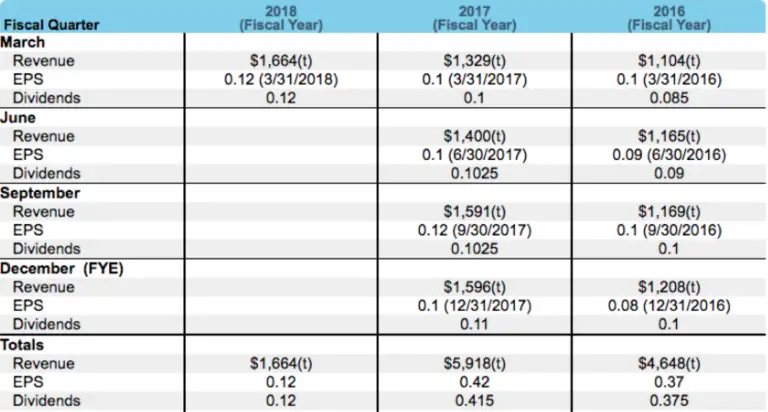

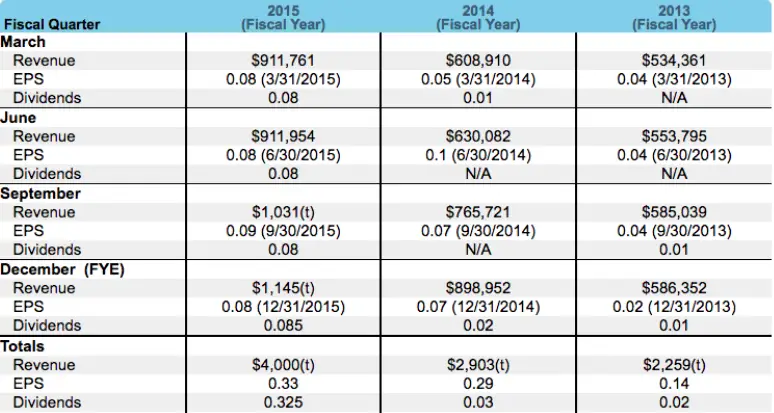

MBC doesn’t have any capex or taxes since it’s a pass-through. So looking at net income is a good proxy for free cash flow. MBC has been reporting an overall trend in increased and positive EPS for the last 5 years.

Source: NASDAQ

In other words, is MBC’s growth attributed solely to injecting fresh capital or is the underlying business’s organic growth fueling the growth? And Public offerings have been at higher stock price each time, i.e. organically increasing retained earnings from the business and the business isn’t growing just from fresh capital

For a financial asset company, I figured P/E and EV/EBITDA multiples and Discounted Cash Flow Method aren’t really going to work. For MBC, I looked at the Price to Book Value (or Net Asset Value in this case). My go-to place to look up general current trading multiples by industry is Professor Damodaran’s page. The closest industries’ P/BV multiples are:

- Financial Services (Non-Bank & Insurance): 2.20x

- REIT: 2.05x

- Real Estate (Development): 1.60x

- Investments & Asset Management: 2.12x

There is no multiple for the exact niche we’re looking for; i.e. hard money lending business, but looking at the proxy industries above, the average P/BV that we should be comparing MBC’s valuation to is about 2.0x.

So, looking at the latest quarterly report ending March 31, 2018, its net asset value/book value is:

Assets $46.856m

Minus:

Intangibles ($0)

Liabilities ($23.635m)

Net Asset Value $23.230m

The company is currently trading at a market cap of $60m. So, the P/NAV (or P/BV) is 2.58x, which is a lot richer than the average industry comparables for P/BV; i.e. MBC’s stock price is quite overpriced at the moment.

The stock could be trading higher as investors are expecting a higher earning and growth in its June quarterly report that’s coming out soon (since today is June 27th, 2018) and a bit of rallying to this point. Also, investors may be buying to meet the shareholder record date in order to meet the ex-dividend date. You must own by July 10, 2018 to be paid on July 16, 2018. The stock price may decline after the ex-dividend date, but I’m greedy and I want a piece of the dividend pie.

9. Any sign of pump & dump?

Three things to look for to detect any sign of pump & dump for a microcap stock is 1) is there a lot of hype around the company? And the answer is no, I haven’t found it online; 2) does the company keep changing names and the direction? And the answer here is no; and 3) are there periods of stock momentum for no reason? There has been an instance of this but really, the company has been reporting higher earnings every quarter, so I would expect it to be attributed to that rather than a pump & dump.

10. Short high interest debt on their balance sheet?

Normally, I don’t like debt but for a hard money lender whose assets are money, using leverage to lend rather than issuing new capital at a high cost of equity is effective as long as the cost of debt is lower. At an average of 6% cost of debt, it’s not too risky to hold debt on its balance sheet.

Additional Rationale to Buy the Stock:

- Requires the borrower to have equity participation

- Requires strong financials of the borrower

- Loans have never defaulted

- Collateral is good – first lien on all real estate developments in New York metropolitan area which is not a market that’s declining anytime soon

- Pays a dividend, which has been steadily increasing

Potential Risks:

- Downturn in the metropolitan New York real estate market

- Loan defaults

- Bad collateral in the case of loan defaults

- Decreasing interest rate

Summary of Analysis

A simple business as a hard money lender. Focuses on the New York metropolitan area which is a hot market and will be for a long time. The CEO and founder has 30% of the stock and he has been with the company through thick and thin since founding it almost 30 years ago. The CEO is scrappy; pivoted the business when he saw a more profitable opportunity. Board members have been with the company for over a decade on average.

The stock is overvalued but on the flip side, is seeing momentum because of consistently reporting higher earnings and growth. The stock also pays a dividend that’s been increasing steadily every quarter, so it’s a nice income stream and diversification to your portfolio. I wrote this post on June 27th at night so am buying on June 28th at a slightly higher price. Damn it.