This post is from 2023. Click here to see the 2024 post.

Hotel Industry Valuation Multiples

There are various methods to value or appraise a hotel, but to get an accurate appraisal, an expert appraiser would be involved.

As with other industries, we can use a simple method of valuation multiples to value the business, which in this case is a hotel.

To analyze the hotel industry valuation multiples, I looked at hotels, motels, resorts, and cruise lines with revenue of at least US$1M in the US, Canada, and the UK. And I removed businesses that lacked meaningful data or were outliers.

Let’s take a look at each set of multiples and infer interesting observations.

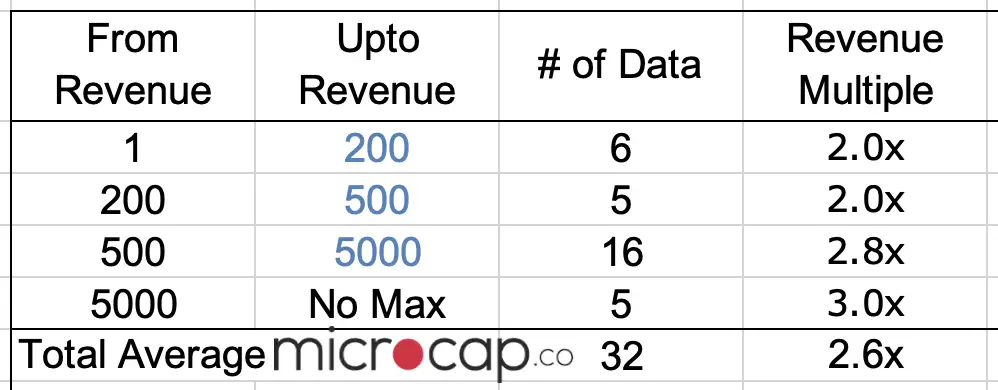

Hotel Revenue Multiple

To calculate valuation multiples, you need the market cap or the enterprise value, which is not available for privately-held companies.

Thus, the average hotel revenue multiple was calculated using only public companies. Out of 32 companies in the data set, the average hotel revenue multiple is 2.6x.

The interesting observation about the average hotel revenue multiple is that I divided up the data set into cohorts of different sizes based on their revenue and this is what I found:

- For companies with revenue in the range of $1 million to $500 million, the average revenue multiple is 2.0x.

- For companies with revenue between $500 million and $5 billion, the average revenue multiple is 2.8x.

- And for companies with revenue larger than $5 billion, the average revenue multiple is 3.0x.

It’s interesting to see that as the size of the company gets larger, their revenue multiple is higher.

As we will see later, this may have something to do with their profitability margins and that hotels gain economies of scale as they get larger and thus are valued higher.

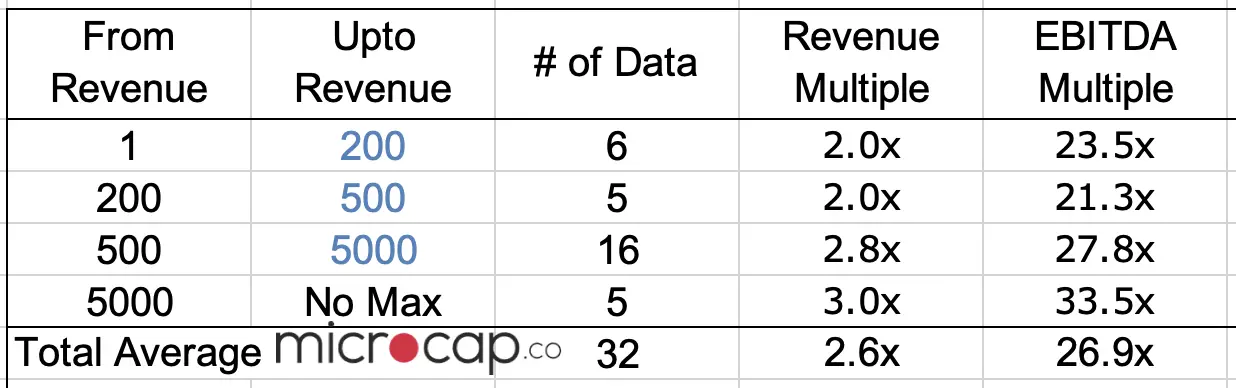

Hotel EBITDA Multiple

Out of the 32 companies in the data set, the average EBITDA multiple is about ~27x.

Between cohorts of companies whose revenue is between $1 million and $200 million and between $200 million and $500 million, there isn’t a clear correlation in the EBITDA multiples like there is for revenue multiples.

Breaking it down by size of companies, this following is a set of observations for the average hotel EBITDA multiple:

- The average EBITDA multiple for companies with revenue between $1 million and $200 million is 23.5x.

- The average EBITDA multiple for companies with revenue between $200 million and $500 million is 21.3x.

- The average EBITDA multiple for companies with revenue between $500 million and $2 billion is 27.8x.

- And, the average EBITDA multiple for companies with revenue larter than $5 billion is 33.5x.

But the larger company cohorts beyond $500 million have higher EBITDA multiples. Again, this is a similar phenomenon to the revenue multiples, which suggests that the companies are valued higher as they get larger.

*Note that the revenue multiple uses the market cap to calculate the multiple whereas the EBITDA multiple uses the enterprise value. This is because EBITDA takes out the effect of debt, so to make it more comparable, we take the enterprise value as the numerator, which takes into account debt and cash of the company.

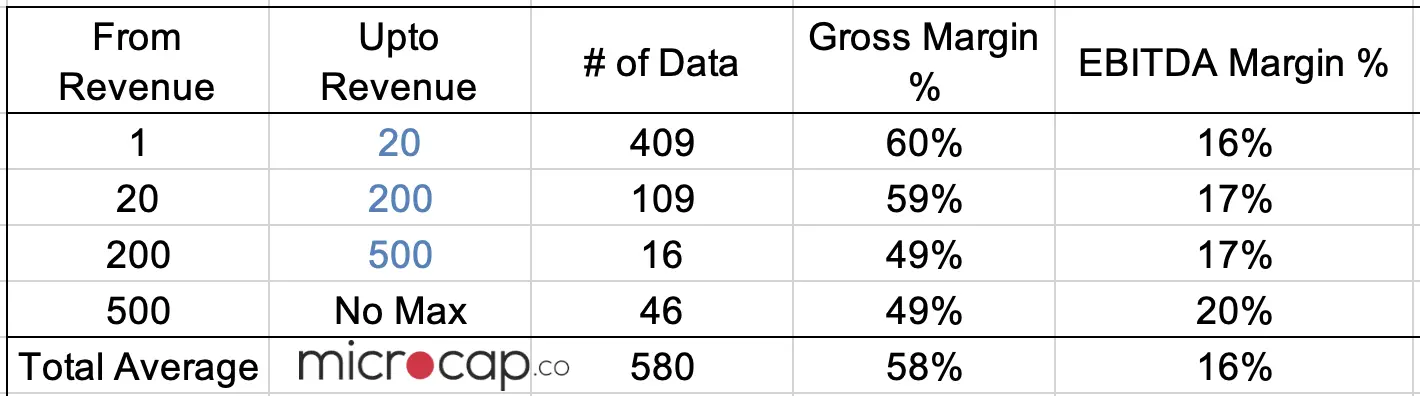

Average Hotel EBITDA Margin

When analyzing only the margins, we don’t need the company’s market cap or enterprise value, so we can look at a larger universe of companies that are not public.

As such, the data set analyzed for average hotel EBITDA margin includes 580 companies, which makes the analysis a lot more reliable with a bigger sample size. (Note for here as well that hotels with outliers or no data were removed from the data set.)

Key observations of the average hotel EBITDA margin:

- The average EBITDA margin for companies with revenues between $1 million and $20 million is 16%.

- The average EBITDA margin for companies with revenues between $20 million and $500 million is 17%.

- The average EBITDA margin for companies with revenues larger than $500 million is 20%.

- Since there are more hotel businesses with smaller revenues (i.e. there are 409 companies in the data set, the average hotel EBITDA margin for the total data set of 580 companies is 16%.

We can start to clearly see the impact of economies of scale when we start observing the EBITDA margin and the gross margin:

- The average gross margin (i.e. revenue minus cost of goods sold) is higher at 60% for smaller companies and decreases to just below 50% for large companies in the data set.

- However, the opposite trend occurs for the average hotel EBITDA margin with smaller companies displaying an average of 16% and the largest hotels of the data set displaying 20%.

This can be explained by a relatively higher operating cost for the smaller companies. That is, because of higher fixed cost, the hotels that have higher revenue are able to take more advantage of the fixed cost and spread it over the business (i.e. more rooms offered).

For example, the building cost, the salaried staff (cleaning staff, management), capital costs such as industrial sized washing machines will have smaller cost per room with more rooms and more revenue earned per room.

And consumable costs such as shampoo, trash bags, or even towels, can be bought at lower-cost in bulk as they buy more at a time.

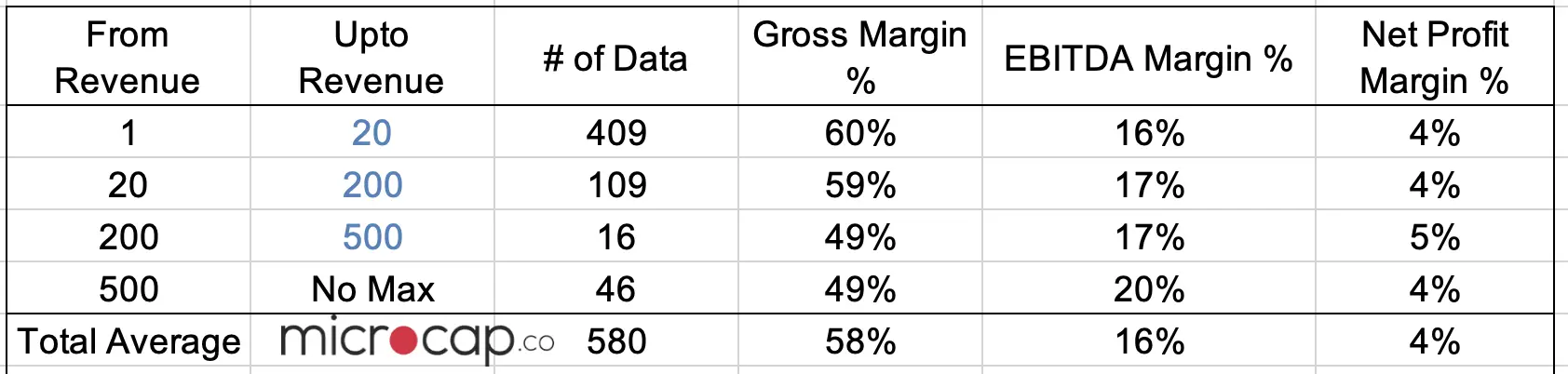

Average Net Profit Margin for Hotel Industry

Now, when we look at the average net profit margin of hotels, the margin for the hotel industry is pretty similar across the size of hotels.

From the data set of 580 companies, the average net profit for the hotel industry is 4%.

It is interesting to see a slight increase in EBITDA margins as the size of hotels increase while the net profit margin stays relatively the same at 4% regardless of the size of the hotels.

There is probably more than one explanation for this, but one reason (which would need to be further studied to know for sure) could lie in the difference between EBITDA and net profit, which is the effect of the capital structure.

What that means is that the net profit (or net income) takes into account the company’s interest for debt as well as taxes and depreciation.

So, as hotels become larger, they may have more debt, for example, which explains higher interest, thereby reducing the relative net profit margin compared to the EBITDA margin.

How To Use Valuation Multiples To Value a Company

For those who are not familiar with using valuation multiples to value companies or those who are but need a refresher, I wrote posts detailing exactly how you can do that.

Hopefully you can use them as helpful guides. Click on the link below to go to the post.

- How to value a company based on revenue

- How to value a company based on EBITDA

- How to value a company based on earnings

- How to find your own valuation multiples

- Other posts on how to value a company

Download Data Set

To download the data set of 580 companies for the average hotel EBITDA margin and the average net profit margin for hotel industry in this analysis as well as the 32 companies analyzed for the average hotel EBITDA multiple, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly.

(I have actually never sent an email to the mailing list, but I may in the future, who knows. But the reason for mailing it directly is because if you can download it with a click of a button, the internet bots go nuts.)

Thanks for reading as always and leave a comment if you found it useful!