In 2024 and the start of 2025, the U.S. insurance industry faced a complex economic landscape.

Property and casualty insurers contended with increased claims due to natural disasters, notably wildfires in California, leading to higher loss ratios and impacting profitability. For instance, Mercury General’s stock declined by 28% amid the Los Angeles wildfires.

Conversely, life insurers experienced steady demand for savings and retirement products, bolstered by consumer concerns over economic uncertainties.

Healthcare insurers, including managed healthcare companies, maintained resilience, though rising medical costs and regulatory challenges influenced their financial performance along with the Unitedhealth CEO incident.

Valuation Multiples for Insurance Companies

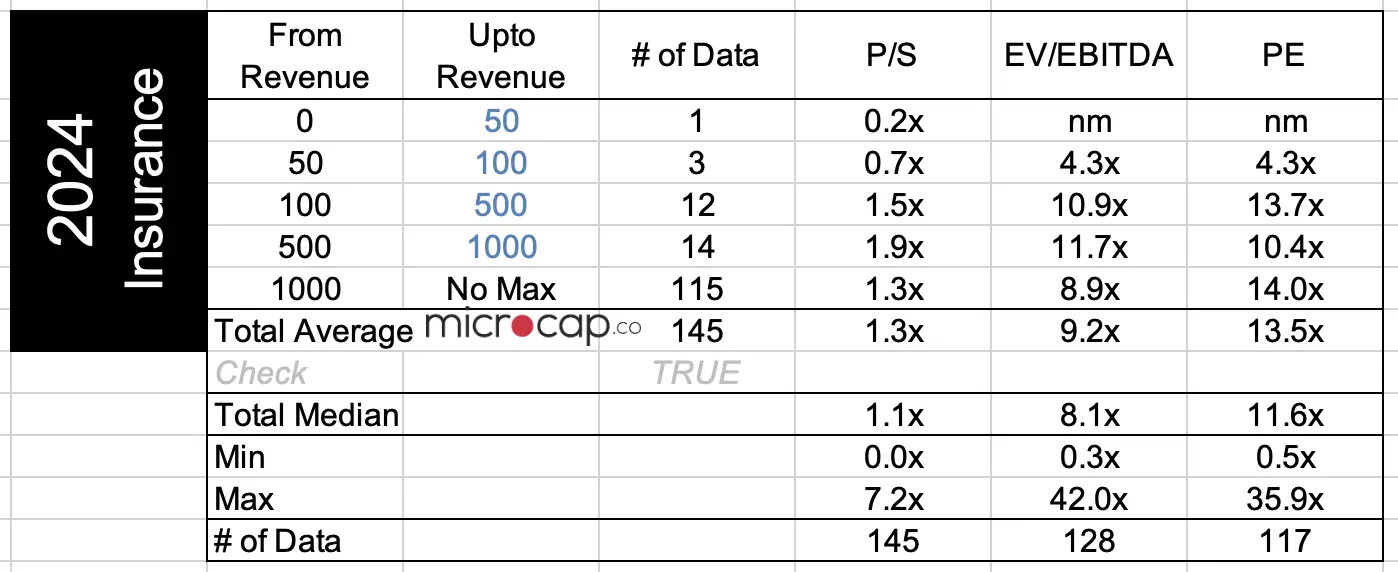

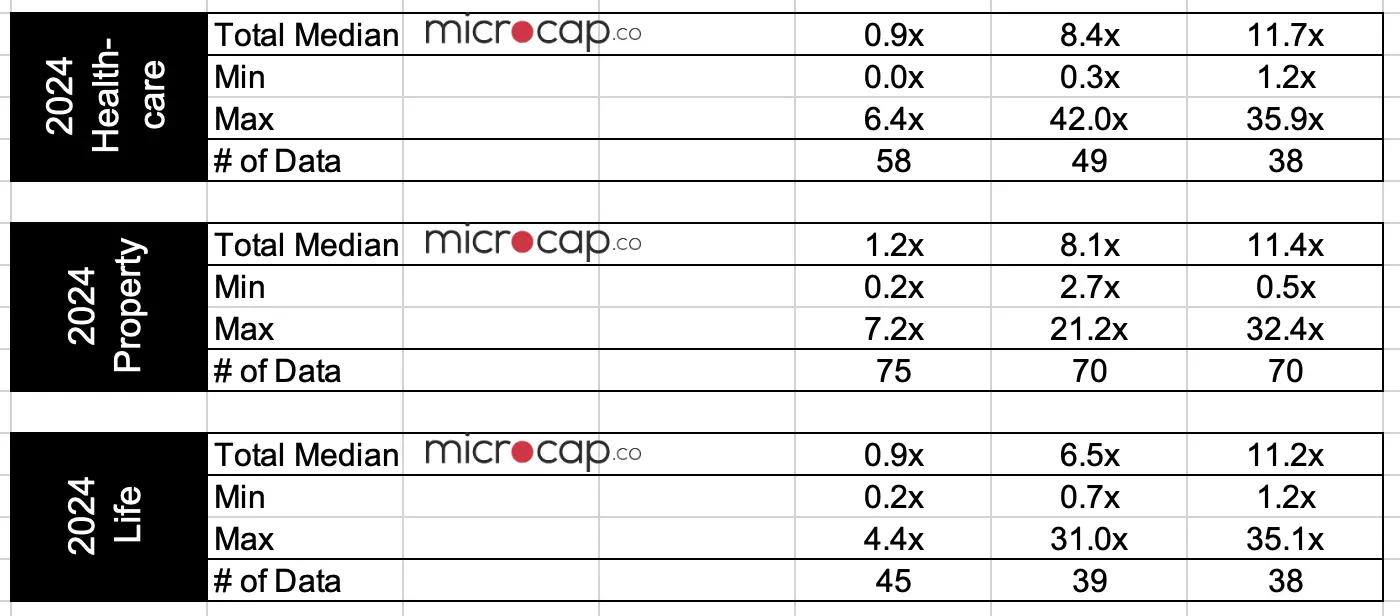

An analysis of 145 public insurance companies, encompassing property and casualty, life, and healthcare sectors, revealed median insurance valuation multiples in 2024 of revenue multiple of 1.1x, EBITDA multiple of 8.1x, and P/E multiple of 11.6x.

Insurance agency valuation multiples remained consistent with 2021 levels during the peak of the pandemic.

These figures align closely with industry norms, reflecting stable investor sentiment.

The uniformity across different insurance sectors suggests that market participants perceive similar risk and return profiles within the industry.

Factors contributing to these valuations include the industry’s inherent stability, regulatory environment, and the ongoing demand for insurance products.

When compared to other industries, these multiples indicate a relatively conservative valuation, consistent with the traditionally steady nature of insurance businesses.

Insurance Companies’ Margins Analysis

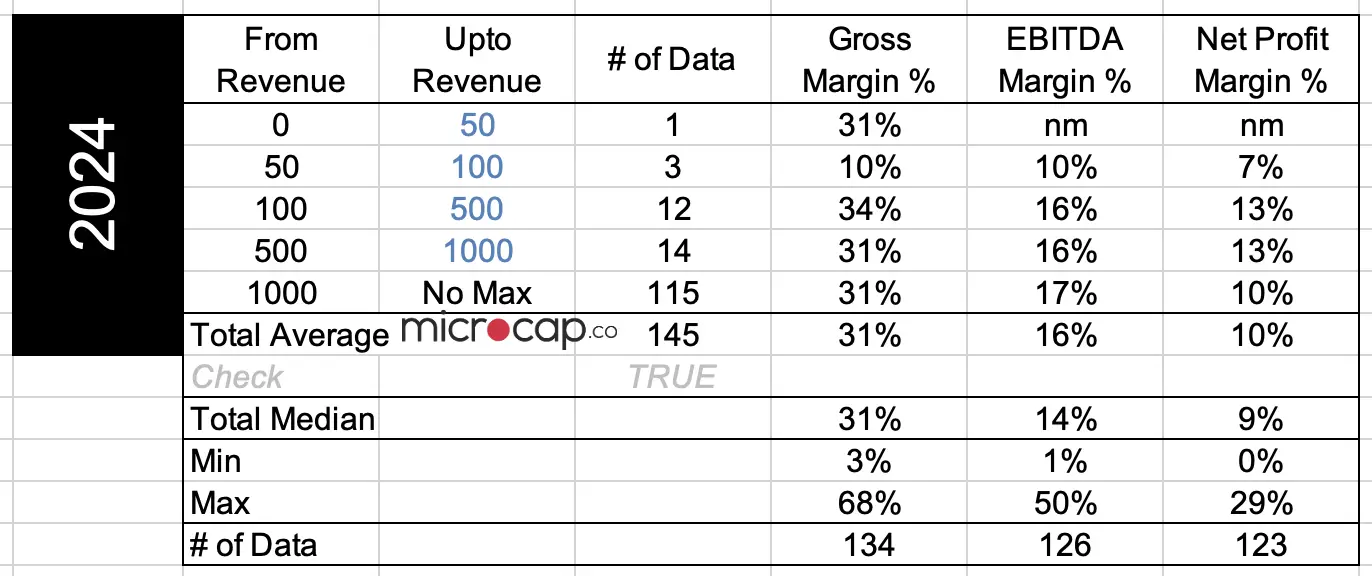

In 2024, the insurance industry reported median gross margin of 39%, EBITDA margin of 10%, and net profit margin of 6%.

These margins reflect the industry’s operational efficiency and risk management practices. The gross margin indicates effective cost control in underwriting and claims management. The EBITDA and net profit margins demonstrate the industry’s ability to maintain profitability despite challenges such as increased claim frequencies and regulatory pressures.

Factors influencing these margins include investment income, expense management, and the competitive landscape.

Insurance Industry Outlook for 2025

Looking ahead, the U.S. insurance industry is expected to navigate several key trends in 2025.

- The increasing frequency of natural disasters may lead to further premium adjustments and a reevaluation of risk models.

- Advancements in technology, particularly in data analytics and artificial intelligence, are anticipated to enhance underwriting processes and customer engagement.

- Regulatory developments will continue to shape industry practices, especially concerning consumer protection and data privacy.

- Additionally, evolving consumer preferences, with a growing emphasis on digital interactions and personalized products, are likely to influence market dynamics.

Download Data Set

To download the 145 companies data set in this analysis, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly. In some cases, it takes a few hours or a day to receive the email with the data set.