[See the latest 2024 data]

In analyzing the real estate company valuation multiples, there were a couple of things to consider.

There are different types of services provided in real estate, so analyzing all real estate companies’ valuation multiples may be skewed incorrectly.

Another challenge of analyzing valuation multiples for real estate companies is that many are private and thus, there isn’t enough data available to calculate the average or median multiples.

Nevertheless, here was my attempt.

To analyze the real estate company valuation multiples, I first screened for public companies in the real estate industry.

After removing companies that had no data or were outliers, I categorized them into 4 sub classifications:

- Real estate agents & brokers

- Real estate operators

- Real estate developers

- Real estate service providers (which includes agents & brokers, appraisers, title service, etc.)

Here is the summary of results.

Real Estate Company Valuation Multiples

All companies in the data set

There were 43 companies in the data set but due to outliers and data that was not available, the different valuation multiples had varying numbers of companies in the data set.

- Out of 43 companies, the median revenue multiple is 1.4x and the average revenue multiple is 1.9x.

- Out of 26 companies, the median EV/EBITDA multiple is 14.1x and the average EV/EBITDA multiple is 15.4x.

- Out of 15 companies, the median PE multiple is 11.5x and the average PE multiple is 13.6x.

- Out of 23 companies, the median EV/earnings multiple is 15.2x and the average EV/earnings multiple is 17.2x.

The next sections are real estate company valuation multiples for different primary services provided.

But you’ll see that there isn’t enough data for many of these valuation multiples to be meaningful.

So, I caution the reliability of these valuation multiples when using it by category.

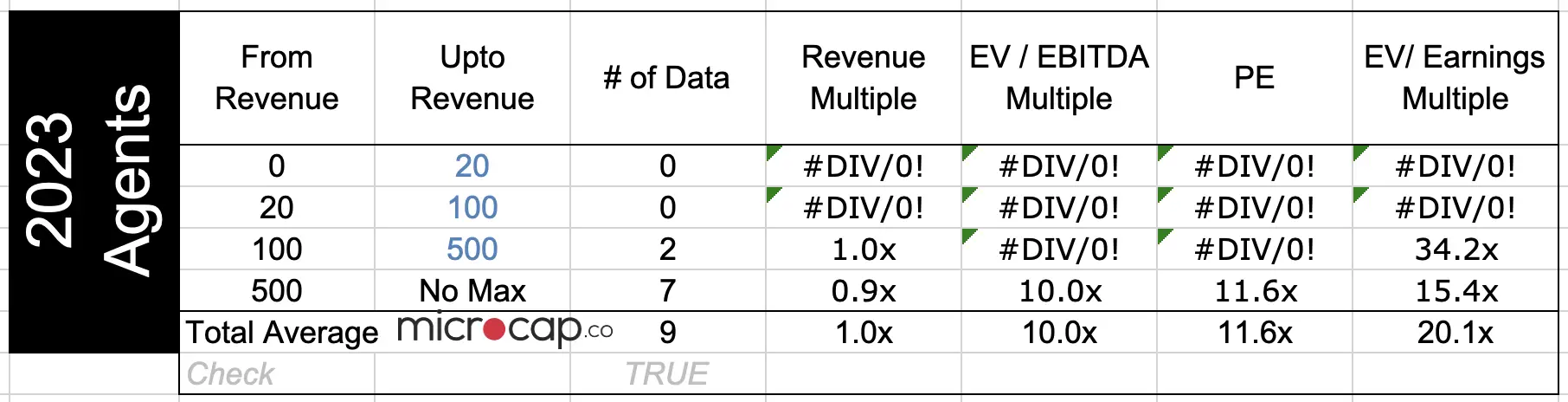

Real estate agents & brokerage companies in the data set

There were only 9 agents & brokers in the data set, so the data is not as meaningful, but nevertheless, the following are the valuation multiples for real estate brokerage companies.

Also note that only large real estate companies that had revenue higher than $300 million identified as agents & brokers had available data.

- The average revenue multiple for real estate agents & brokerage companies is 1.0x.

- The average EV/EBITDA multiple for real estate agents & brokerage companies is 10.0x.

- The average EV/earnings multiple for real estate agents & brokerage companies is 20.1x.

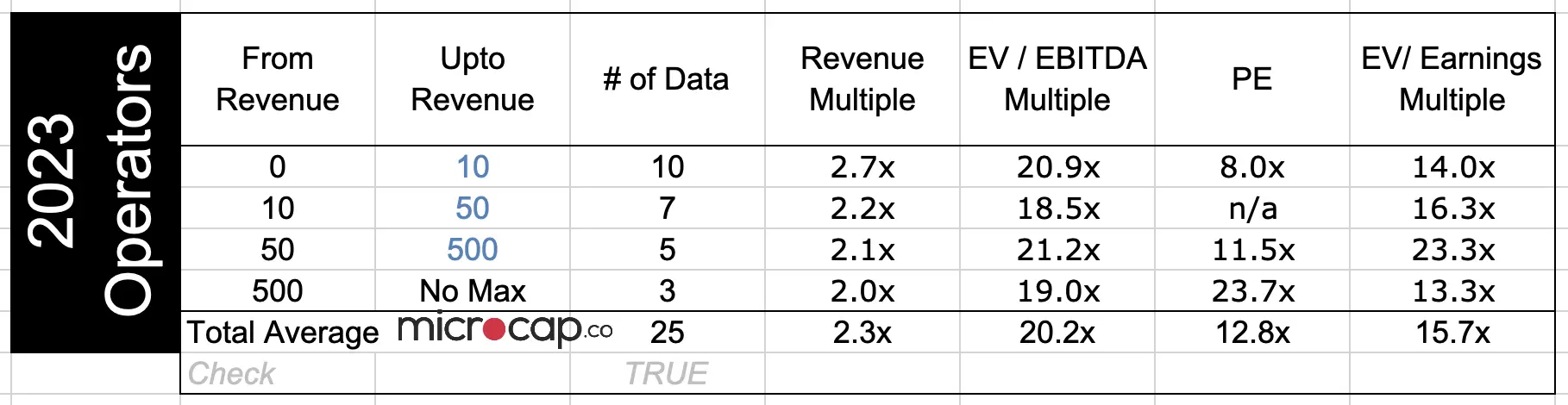

Real estate operators in the data set

There were a number of smaller real estate operators (17 of which have less than $50 million in revenue), which would include real estate operators managing multiple residences or smaller commercial buildings.

- The average revenue multiple for real estate operators is 2.3x.

- The average EV/EBITDA multiple for real estate operators is 20.2.

- The average EV/earnings multiple for real estate operators is 15.7x, which is lower than EV/EBITDA, and this does not make sense to me. There is probably inaccurately reported data that is pulling this multiple the wrong way.

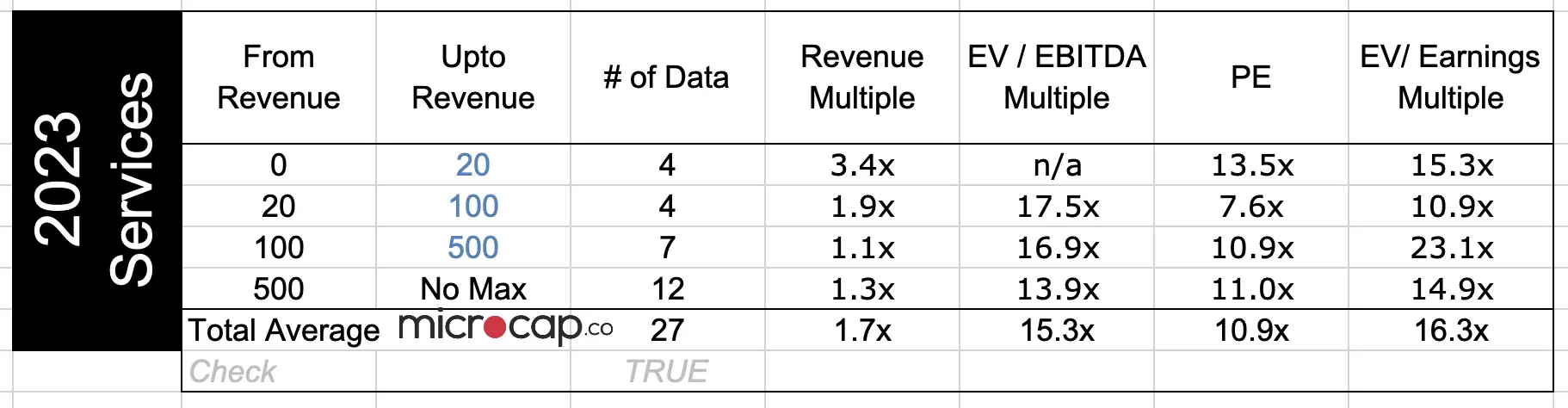

Real estate service providers

This category of real estate service providers include services such as brokerage, appraisal, titles, and other.

The multiples below are a summary of all the real estate service providers in the data set.

- The average revenue multiple for real estate service providers is 1.7x.

- The average EV/EBITDA multiple for real estate service providers is 15.3x.

- The average EV/earnings multiple for real estate service providers is 16.3x.

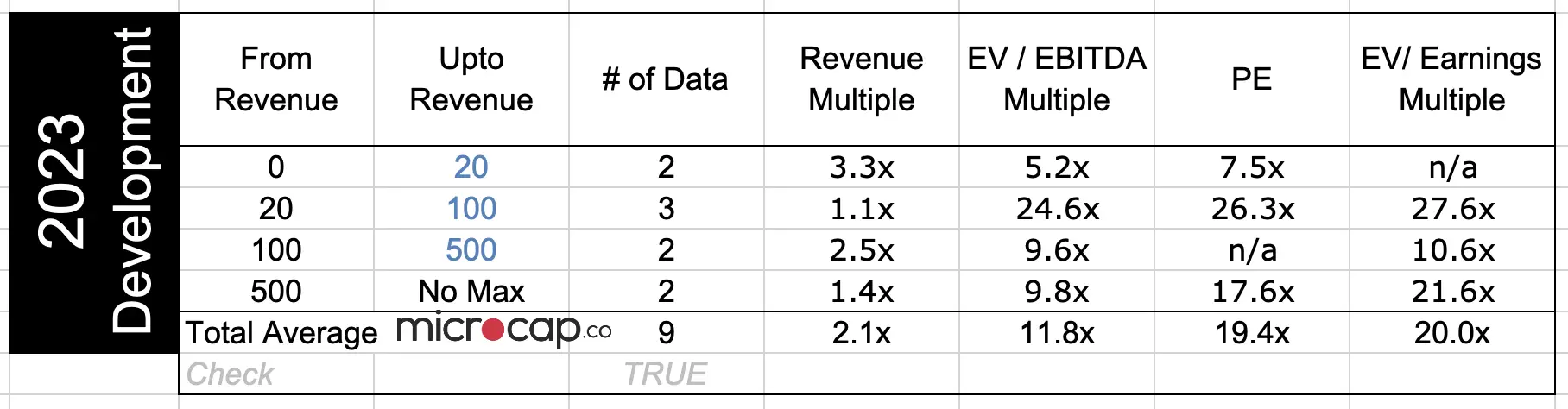

Real estate development companies

Finally, we have real estate development companies.

This category also has very few companies in the data set, so the multiples won’t be very meaningful.

- The average revenue multiple for real estate developers is 2.1x.

- The average eV/EBITDA multiple for real estate developers is 11.8x.

- The average EV/earnings multiple for real estate developers is 20.0x.

How to Value a Real Estate Development Company

A word of caution: valuing a real estate development company isn’t as straightforward as taking the industry’s average EBITDA multiple for example and multiplying it to the company’s EBITDA.

Interest rates kept rising in 2023, which is a huge factor in valuing the sector.

When it comes to real estate developers, valuing the company involves analyzing the value of the real estate development projects that the company has already completed or is currently working on.

This includes looking at factors such as the market value of the land and buildings, the cost of construction, the expected cash flows from rent, and any other potential returns from the project.

Additionally, it is important to consider the company’s potential for future growth, as well as any potential risks that may be associated with the development projects.

On the other hand, valuing a real estate management company is different from valuing a real estate development company, as it involves looking at the company’s day-to-day operations.

This includes analyzing the management fees that the company charges, the amount of rent collected, the occupancy rate of the properties, and the profitability of the company.

It’s important to consider the company’s potential for growth and any potential risks associated with the management of the properties.

How To Use Valuation Multiples to Value a Company

For those who are not familiar with using valuation multiples to value companies, I wrote posts detailing exactly how you can do that.

Hopefully you can use them as helpful guides. Click on the link below to go to the post.

- How to value a company based on revenue

- How to value a company based on EBITDA

- How to value a company based on earnings

- How to find your own valuation multiples

- Other posts on how to value a company

Download Data Set

To download the data set of the companies in this analysis, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly. In some cases, it takes a few hours or a day to receive the email with the data set.

(I have never sent an email to the mailing list, but I may in the future, who knows. But the reason for mailing it directly is because if you can download it with a click of a button, the internet bots go nuts.)

Thanks for reading as always and leave a comment if you found it useful!