[Note: This analysis includes only SaaS companies. For the analysis of the broader tech software industry, see the 2024 tech software companies valuation post. For older data, see the 2019 post.]

Software companies are not all software-as-a-service (SaaS) companies.

SaaS companies deliver a cloud-based software on a subscription model, with recurring revenue for the software vendor and low upfront costs for customers as the unique characteristics of SaaS.

And due to the low cost nature for customers, the opportunity for SaaS is its scalability.

Below is not an exhaustive list, but example non-SaaS software companies for illustration:

- Infrastructure software: the backbone of IT systems, which enables database management, cloud platforms, IT infrastructure networks. E.g. companies like VMware, Oracle, Microsoft Azure.

- Enterprise software: enables complex needs of large organizations to manage the business operations and organizational workflows like enterprise resource planning (ERP). E.g., companies like SAP, Workday, ServiceNow.

- Cybersecurity software: solutions for threat detection, prevention, response, to protect sensitive data and systems. E.g., companies like Palo Alto Networks, CrowdStrike.

- Developer tools and platforms: tools and platforms for software developers to use, create, test, deploy apps. E.g., companies like GitHub, Atlassian, Visual Studio.

- E-commerce and marketplace software: Backend platforms that provide online shopping infrastructure. E.g,, companies like Shopify, Magento, Etsy.

For this analysis, I wanted to see if pure-play SaaS companies have higher valuation multiples compared to other tech software companies. The rationale would be that they command a premium for the recurring revenue and scalability aspect.

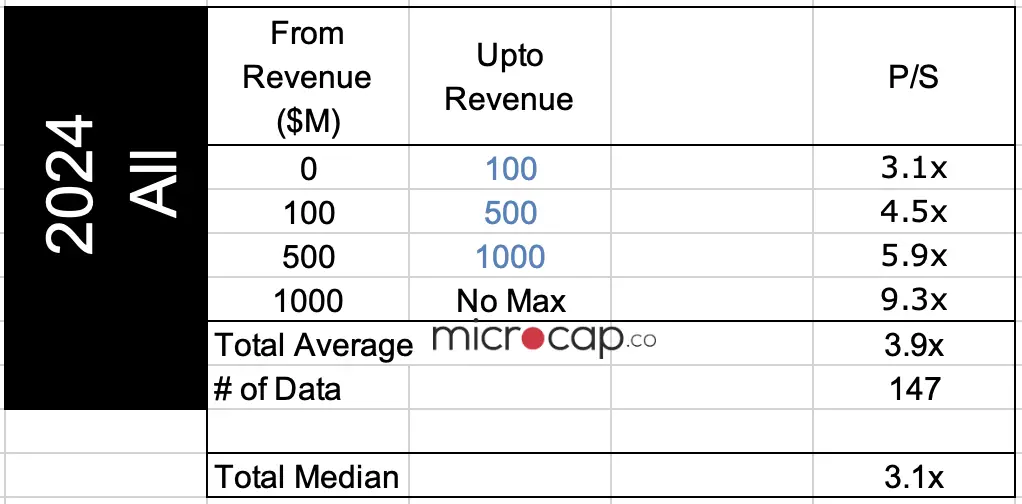

SaaS Revenue Multiples

Recall from the tech software companies valuation multiples, the global average P/S multiple for all market cap size is 3.4x.

Comparatively, SaaS only companies average is 3.9x and median is 3.1x out of 147 companies in the dataset. Taking the mid point of the average and median, the revenue multiple is ~3.5x.

The difference between 3.5x and 3.4x is too close to characterize SaaS companies as having higher valuation multiples.

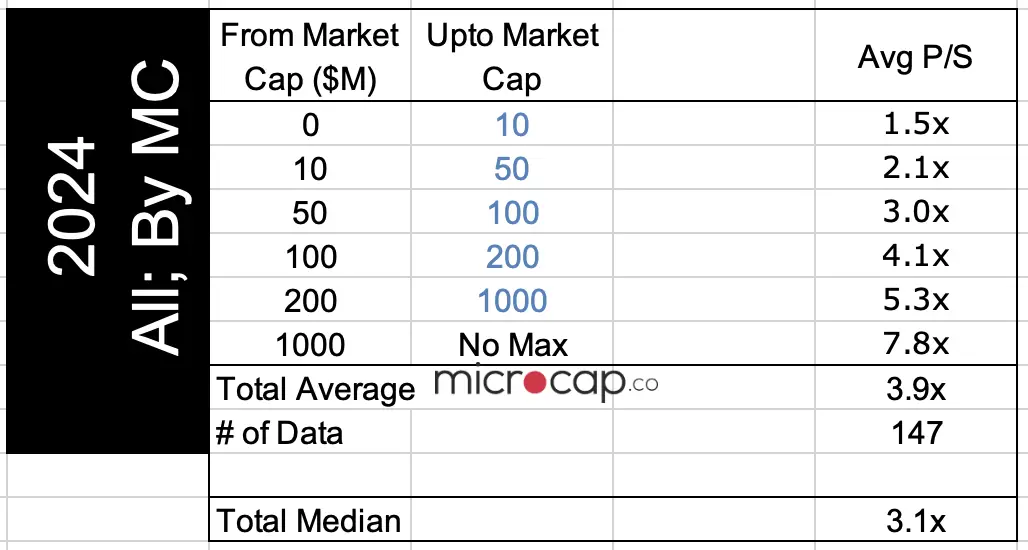

The first table above breaks down the SaaS companies’ revenue multiples by annual revenue and the second table breaks down the multiples by market cap size. In both scenarios, it’s interesting and expected to see that as the company size increases, the company’s revenue multiples are given a higher valuation.

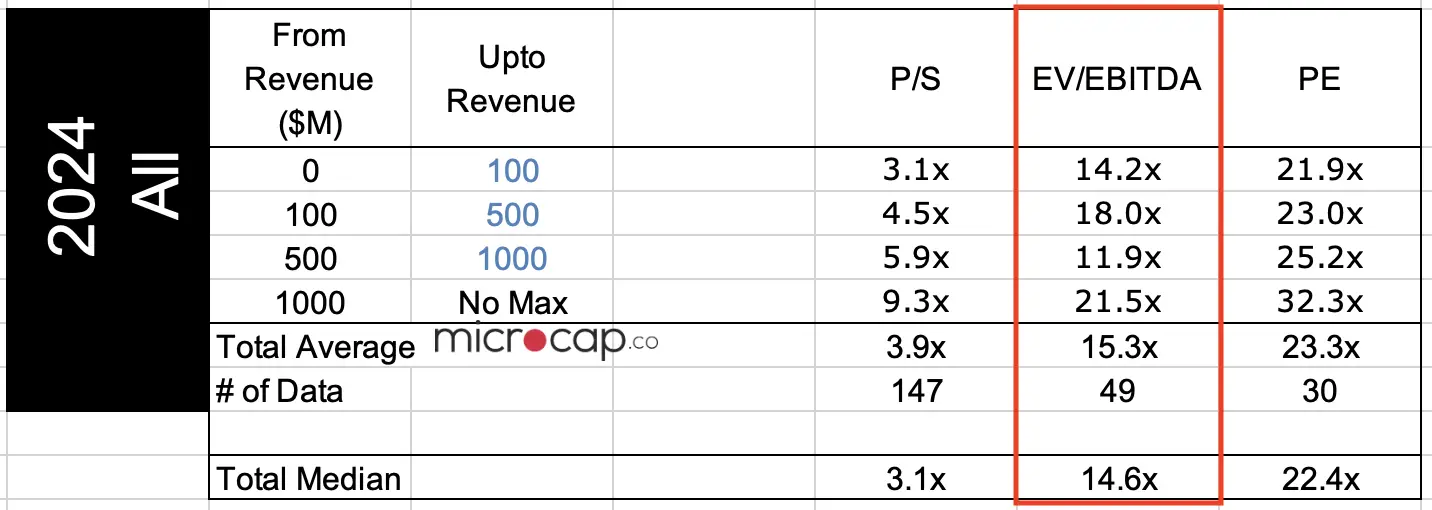

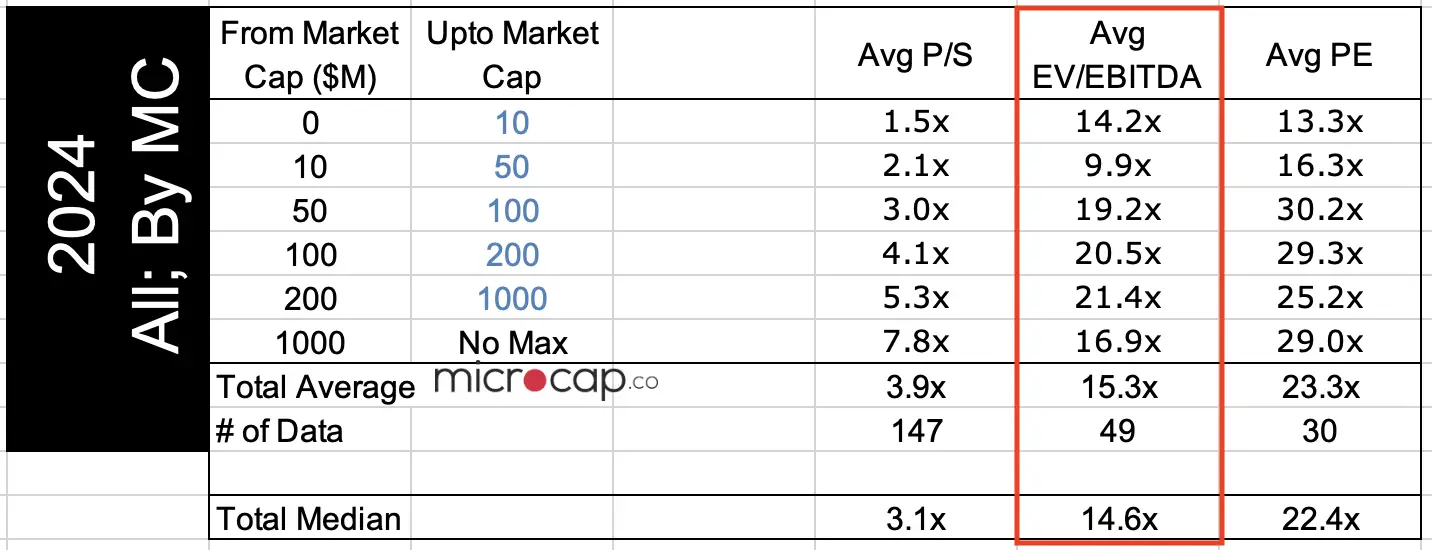

SaaS Company Multiple EBITDA

As for the EBITDA multiples, the global average EV/EBITDA multiple for all tech software companies is 22.1x.

Comparatively, EBITDA multiples for SaaS only companies is ~15.0x (midpoint between 15.3x average and 14.6x median).

Why do SaaS companies have a lower EBITDA multiple compared to other software companies but a similar revenue multiple? Many factors can be contributing to this observation, but here’s my conjecture.

- SaaS companies have recurring revenue, which the market likes. SaaS companies are expected to have revenue growth annually to scale. This is the most important aspect of SaaS companies.

- Profitability of SaaS companies depends on scalability, so again, scalability is the critical factor.

- For that reason, investors anchor their valuation of SaaS companies on revenue multiples more than EBITDA multiples. So, even if EBITDA profitability was higher for SaaS companies relative to all software companies, the valuation will be anchored on the revenue.

- On the other hand, for overall software companies, profitability is garnered as the more important valuation metric by investors.

SaaS Company Valuations in 2025

With that in mind from 2024, what do we need to look out for in 2025 specifically for SaaS companies?

- Investors are placing high value on consistent and predictable recurring revenue streams. Achieving high revenue growth and higher and consistent annual recurring revenue (ARR) will be critical for SaaS companies to get higher valuation.

- Improving profitability will continue to be a focus for investors when they assess tech companies, but not as important as revenue growth for SaaS company valuations. Nonetheless, failure to keep the profitability stable or increasing will have deteriorate all software company valuations. For SaaS companies in particular, lowering customer acquisition cost (CAC) will be attractive to investors as well as operational efficiency to burn less cash.

Download 2024 Data

To download the dataset consisting of 44 companies in this analysis, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly. In some cases, it takes a few hours or a day to receive the email with the data set.