In 2024, the valuation landscape for software companies experienced a large shift influenced by various factors. For 2023 post, click here. Or if you want SaaS only company valuations, go here.

As you’ll see in the analysis below, valuation multiples of tech software companies recovered from a decline in 2023. It’s been a bit of a roller coaster with a dip at the start of the pandemic to a huge leap soon after, then a decline in 2021, recovery in 2022, downward shift in 2023, and now back up to its height.

Some factors that may have contributed to the increase in valuation multiples:

- A focus on AI technologies by software companies globally and some showing successful AI integration into their softwares drove growth, innovation, and investor optimism.

- Expectations of interest rate reductions contributed to increased valuations. Lower borrowing costs are generally favorable for tech investments, leading to heightened investor interest and higher valuation multiples.

- The software sector witnessed a rise in M&A transactions, particularly within the cybersecurity domain. Investors anticipate an increase in mergers in 2025, as larger vendors seek to expand their portfolios amid a decline in venture capital funding.

- Stock prices were elevated, but comparing the forward PE ratios, the valuation appeared reasonable, which suggests that earnings growth expectations were justified. Investors are cautious but optimistic going into 2025.

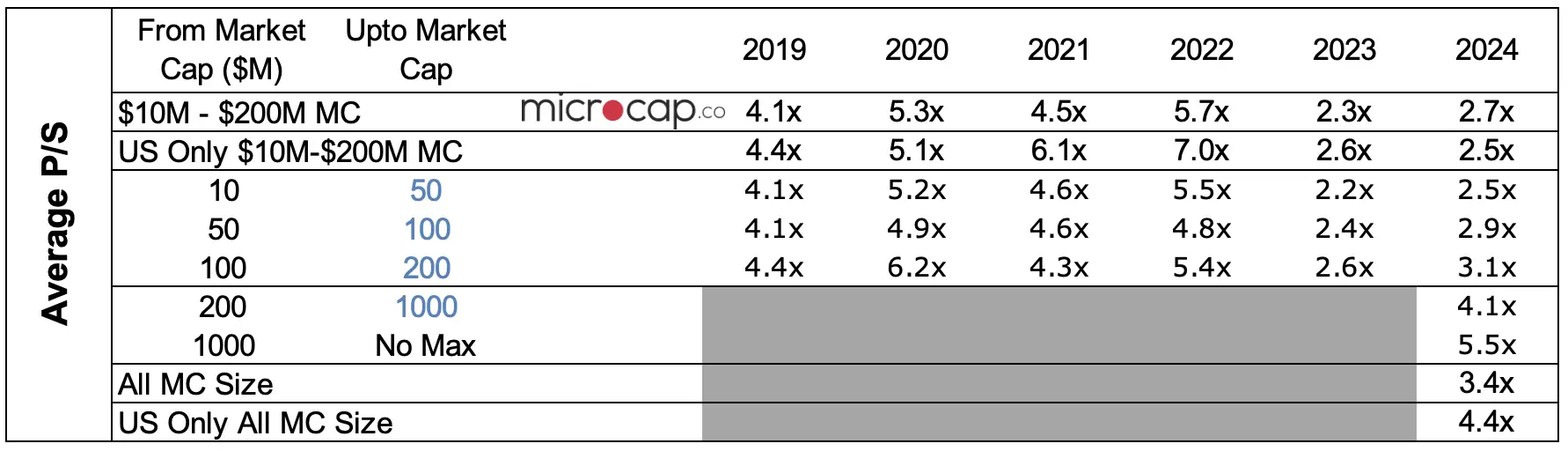

Software Company Valuation Revenue Multiple

As explained in my 2019 post post, the revenue multiple is a widely used valuation multiple for tech companies, because tech companies are not profitable when they start due to the high amount of investment, which takes time to pay back.

In my analysis, I remove outliers on either ends such that the average and median are in a proximate range. The first thing I noticed in the 2024 data was that there was a lot more disparity between the lowest multiples and highest revenue multiples relative to previous years. For example, if there are only a few numbers that are above 30x, then I would remove them. But in this year’s dataset, there were too many numbers in the high range to call them outliers.

Due to this reason, I used the trimming method instead whereby I removed the bottom 10% and top 10% of the revenue multiples dataset.

In previous years, I focused on companies with market cap between $10M and $200M. From 2024 onward, I will also include all market size public companies.

Revenue multiples trend commentary:

- Smaller software firms within the $10 million to $200 million market cap range experienced a modest recovery in average price-to-sales (P/S) ratios, increasing from 2.3x in 2023 to 2.7x in 2024. This improvement suggests a stabilization in investor sentiment following the significant declines observed in 2023.

- US-based companies in the same market cap bracket saw a slight decrease in P/S ratios, moving from 2.6x in 2023 to 2.5x in 2024. The decline is too small to indicate any notable changes in the market or companies, but the fact that they did not move in the same direction compared to the global landscape indicates that U.S. firms may be facing more unique challenges, such as increased competition or market saturation.

- The general trend across the software industry in 2024 points to a stabilization of valuation multiples after the volatility of previous years. Factors contributing to this equilibrium include advancements in artificial intelligence, strategic mergers and acquisitions, and a focus on sustainable growth and profitability.

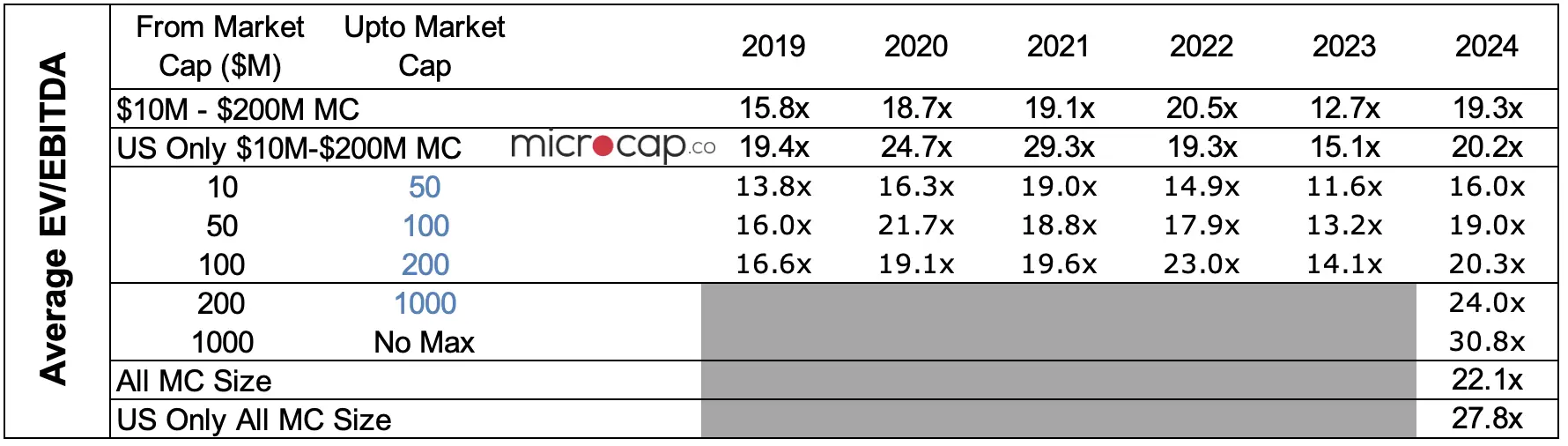

Software Company EBITDA Multiples

In 2024, the EV/EBITDA multiples for software companies across different market cap ranges showed significant rebounds after sharp declines in 2023. Here’s a breakdown of the trends and insights by market cap range.

EBITDA multiples trend commentary:

- For software companies with market caps between $10M–$200M, the average EV/EBITDA multiple rose from 12.7x in 2023 to 19.3x in 2024. This recovery signals a resurgence in investor confidence, possibly driven by improving profitability metrics and a stabilization in broader market conditions after macroeconomic volatility in 2023. Investors appeared to have expectations of stronger EBITDA performance.

- US-based software companies in the $10M–$200M market cap range saw EV/EBITDA multiples increase from 15.1x in 2023 to 20.2x in 2024. This recovery, though slightly less pronounced compared to global averages, highlights the U.S. market’s ability to attract premium valuations despite economic headwinds such as inflation and higher interest rates. The rebound reflects a re-alignment of valuations with the perceived long-term stability of U.S.-headquartered companies.

- Looking at the US companies data only provides a very interesting dynamics at play. The revenue multiple declined slightly from 2.6x to 2.5x but EBITDA multiple increased from 15.1x to 20.2x. What could that mean? This most likely suggests that investors are aligning their valuation with profitability more than revenue growth. This is a departure from past expectations of investors where for tech companies, the most critical factor was revenue growth. While revenue growth is a trait that continues to be what investors expect for tech companies, the shift seems to be a favorability of tech companies to prove their profitability.

Valuation Changes in 2025 for Tech Companies

Here’s what to look out for in the coming year:

- More emphasis on profitability than hyper revenue growth.

- Tech companies are anticipated to move away from stock-based compensation toward cash-based pay. This change is driven by rising interest rates and a market focus on profitability. This could impact company valuations.

- Increase in M&A transactions amid a decline in venture capital funding. This consolidation trend reflects strategic moves to enhance market positioning and operational capabilities.

- Investors want to see the ROI pay off of integrating AI into the products. Valuation premium may be given to companies that can successfully integrate AI-driven automation into their products and services.

- The incoming administration’s plans to implement substantial tariffs on imports could impact tech companies reliant on global supply chains. For instance, proposed tariffs on Chinese goods may affect firms like Apple, which depend on Chinese manufacturing. These policies could lead to increased operational costs, potentially affecting profit margins and valuations on US software companies that rely on foreign imports.

- This one is very speculative but worth a mention; i.e. the establishment of the Department of Government Efficiency (DOGE), led by figures such as Elon Musk.

- There could be streamlined regulations and potentially reduced bureaucratic hurdles when it comes to investing in tech innovation.

- But, the DOGE initiative aims to cut $2 trillion in government spending over the next decade.

- It’s unsure if the DOGE initiative will be a positive or a negative for tech software companies.

- Anticipated tax reforms, including the potential extension of the 2017 Tax Cuts and Jobs Act (TCJA) and adjustments to corporate tax rates, could influence investment decisions within the tech sector. Lower effective corporate tax rates for domestic production may increase after-tax profits for software companies, potentially leading to higher valuations.

Download 2024 Data

To download the dataset consisting of 1,030 companies in this analysis, enter your email address below to sign-up for the mailing list and the data set will be sent to your email directly. In some cases, it takes a few hours or a day to receive the email with the data set.