This post was written in 2019. A lot has happened since then, so here’s an updated article written in 2023 with updated valuation multiples for software companies. You’ll find more information about the multiples themselves in this article. And you can find the updated multiples in the 2023 article. See updated 2024 numbers.

Valuing software companies is similar to valuing other companies, but there are some differences such as which valuation multiples to use.

Here, we will discuss the appropriate valuation multiples for software companies and what the average multiples are based on analyzing more than 450 public companies.

Valuation Multiples For Software Companies

The two most popular valuation multiples for software companies are Price to Sales (P/S) and EV/EBITDA.

Many software companies operate at a loss until they scale to a large enterprise. For that reason, you see negative net income and a lot of the times, negative EBITDA.

So, it’s especially important for smaller companies to look at valuation multiples above the net income line.

And because of the negative earnings and EBITDA, another multiple that is widely used is price to sales (P/S) multiples, which is also known as revenue multiples.

Price to sales multiple is basically market cap divided by the company’s revenue. Since revenue can’t be below 0, it’s a functional way to compare all software companies with sales greater than 0.

EV/EBITDA multiple, also known as EBITDA multiple, is a very widely used valuation multiple for companies across almost all industries. And, it’s no different here.

Even though negative EBITDA reduces the number of software companies you can use in the data set, it’s still a good encapsulation of how well the company is doing in comparison to others in the industry.

We looked at a total of 455 public software companies with a market cap between $10 million and $200 million in various sectors across countries.

Here are our findings for average valuation multiples for software companies.

Average Revenue Multiples for Software Companies

After analyzing 455 software companies, we found that the average revenue multiple, i.e. price to sales multiple, is about 4x times.

So, if you want to value a private software company, you can multiply 4 by the company’s revenue to get a rough estimate of its valuation.

This was consistent across US software companies, foreign software companies, and software companies with a market cap of less than $50 million or up to $200 million.

[one_half_first]YourContentHere[/one_half_first][one_half_last]YourContentHere[/one_half_last]

Mega software companies were acquired on average at 4.5x multiple of revenue according to EY’s 2017/2018 report.

And as you can see in this set of findings, smaller companies have a slightly lower average price to sales multiple, but is not too far off.

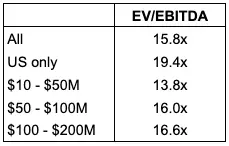

Average EBITDA Multiples for Software Companies

First, we eliminated the companies with negative EBITDA from the data set. As a result, we used 293 in our data set.

EBITDA multiples are Enterprise Value divided by EBITDA. This means you can multiply the EBITDA multiple by a private software company’s EBITDA to estimate the company’s valuation.

For smaller companies whose market cap is between $10 million and $200 million, the average EBITDA multiple is ~16x times.

US software companies exhibit a higher average EBITDA multiple of 19x times.

And the smallest of the small companies whose market cap is between $10 million and $50 million, had lower average EBITDA multiple of 13.8x times. This suggests that because smaller companies are not profitable or as profitable as large, scaled companies, the market values them less, which drags down the multiple.

The mega software companies were acquired at around 21x times EBITDA multiples, so it’s clear that the market is more cautious with smaller companies.

Summary

Price to sales multiple and EV/EBITDA multiple are widely used to value software companies quickly.

An average of 4.0x price to sales multiple and an average of 16.0x EV/EBITDA multiple can be used to value smaller software companies.

These methods should be used in conjunction with other valuation methods, such as forecasting the company’s revenue through to its cash flow over multiple years.

Below is the dataset used in the analysis. I hope you found this useful. If so, leave me a comment or share with someone who can also benefit from this post!

Sample Dataset

Below is the sample dataset of the US public software companies used in the analysis above [in the March 2019 analysis]. See the 2023 updated post to download the full data set.

| Company Name | Year Founded | Price to Sales | EV/EBITDA |

| Synacor, Inc. (NasdaqGM:SYNC) | 1998 | 0.5x | |

| Vobile Group Limited (SEHK:3738) | 2005 | 11.0x | |

| Intelligent Systems Corporation (AMEX:INS) | 1973 | 17.5x | |

| Inuvo, Inc. (AMEX:INUV) | 1987 | 0.6x | |

| Nxt-ID, Inc. (NasdaqCM:NXTD) | 2011 | 1.1x | |

| Accelerize Inc. (OTCPK:ACLZ) | 2001 | 0.4x | |

| AudioEye, Inc. (NasdaqCM:AEYE) | 2005 | 28.6x | |

| SharpSpring, Inc. (NasdaqCM:SHSP) | 1998 | 6.6x | |

| Vertical Computer Systems, Inc. (OTCPK:VCSY) | – | 3.3x | |

| TrackX Holdings Inc. (TSXV:TKX) | – | 5.0x | |

| ImageWare Systems, Inc. (OTCPK:IWSY) | 1987 | 26.4x | |

| Smith Micro Software, Inc. (NasdaqCM:SMSI) | 1982 | 2.5x | |

| CYREN Ltd. (NasdaqCM:CYRN) | 1991 | 3.4x | |

| SITO Mobile, Ltd. (NasdaqCM:SITO) | 2000 | 1.2x | |

| Corero Network Security plc (AIM:CNS) | 1991 | 5.9x | |

| RealNetworks, Inc. (NasdaqGS:RNWK) | 1994 | 1.8x | |

| Duos Technologies Group, Inc. (OTCPK:DUOT) | 1990 | 3.2x | |

| Qumu Corporation (NasdaqCM:QUMU) | 1978 | 0.9x | |

| Investview, Inc. (OTCPK:INVU) | – | 2.1x | |

| Net Element, Inc. (NasdaqCM:NETE) | 2004 | 0.4x | |

| BIO-key International, Inc. (NasdaqCM:BKYI) | 1993 | 2.3x | |

| Veritone, Inc. (NasdaqGM:VERI) | 2014 | 5.0x | |

| BSQUARE Corporation (NasdaqGM:BSQR) | 1994 | 0.3x | |

| Marin Software Incorporated (NasdaqGM:MRIN) | 2006 | 0.4x | |

| MGT Capital Investments, Inc. (OTCPK:MGTI) | 1979 | 3.5x | |

| Finjan Holdings, Inc. (NasdaqCM:FNJN) | 1997 | 1.7x | 1.2x |

| OneMarket Limited (ASX:OMN) | 2017 | 22.8x | 1.6x |

| Evolving Systems, Inc. (NasdaqCM:EVOL) | 1985 | 0.6x | 2.0x |

| Support.com, Inc. (NasdaqCM:SPRT) | 1997 | 0.8x | 3.4x |

| SeaChange International, Inc. (NasdaqGS:SEAC) | 1993 | 0.6x | 6.8x |

| NetSol Technologies, Inc. (NasdaqCM:NTWK) | 1997 | 1.6x | 10.8x |

| EXEM Co., Ltd. (KOSDAQ:A205100) | 2001 | 2.6x | 11.1x |

| SilverSun Technologies, Inc. (NasdaqCM:SSNT) | 1988 | 0.5x | 11.9x |

| Fasoo.Com Co., Ltd. (KOSDAQ:A150900) | – | 1.2x | 13.1x |

| Issuer Direct Corporation (AMEX:ISDR) | 1988 | 3.7x | 14.2x |

| MAM Software Group, Inc. (NasdaqCM:MAMS) | – | 3.0x | 20.1x |

| Intrusion Inc. (OTCPK:INTZ) | 1983 | 5.3x | 21.8x |

| Asure Software, Inc. (NasdaqCM:ASUR) | 1985 | 1.7x | 22.9x |

| GSE Systems, Inc. (NasdaqCM:GVP) | 1994 | 0.9x | 23.2x |

| FalconStor Software, Inc. (OTCPK:FALC) | 1989 | 1.2x | 24.8x |

| GlobalSCAPE, Inc. (AMEX:GSB) | 1996 | 3.0x | 31.7x |

| Park City Group, Inc. (NasdaqCM:PCYG) | 1990 | 6.9x | 34.3x |

| Weyland Tech Inc. (OTCPK:WEYL) | – | 1.2x | 36.1x |

| Aware, Inc. (NasdaqGM:AWRE) | 1986 | 5.4x | 43.4x |

| Where Food Comes From, Inc. (OTCPK:WFCF) | 1996 | 3.1x | 54.0x |

| Astea International Inc. (OTCPK:ATEA) | 1979 | 0.9x |

May I have a full list of your sample companies use in your analysis please?

Thanks for your question, Min. I’ll include the companies in the articles going forward. Thanks for your feedback!

Hi Min! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Dear Sir/ Madam

I liked your article on software company valuation, Please could you email me the complete dataset of 455 companies used in the analysis?

Thank you in advance

Regards

Fon

Hi Fon, thanks for your feedback; I will include the data set in the article going forward.

Hi Fon! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Would love to get the full data set. Thank you!

Hi Mike, thanks for your feedback. I will include the data set going forward.

Hi Mike! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Nice analysis… I’d like to see your complete data set. Did you include non-public companies in your analysis? Do you have a breakdown by SaaS and or ‘blockchain’ related?

Hi Mark, thanks for your feedback. I will include the data set going forward.

Hi Mark! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software. They are all public.

Hi, that’s an amazing review, could you send the full dataset?

Hi Gustavo! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Hi, thanks for the article above! Could you send me the full dataset with multiples? I assume those are only trading multiples and not transaction multiples. Is that correct? Do you also have transaction multiples? And multiples on European software companies ?

Thanks

Hi Alex! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software. Some are European software companies. I’ve included the HQ country of the companies. And yes, they are trading multiples, not transaction multiples. I’ll add that to my list to post in the future.

Great read, would I be able to get the data set?

Hi David, thanks for your comment! The companies used in the analysis and their multiples are listed in the article above.

Hi David! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Hi Microcap: this is a really useful analysis. I’d like to see the complete dataset so that I can look focus on the companies that are in particular software segments. Thank you!

Thanks for your comment, Mary! I’ve gotten a lot of questions on this. I will post an updated software company valuation list. If you want to be notified, please sign up for the mailing list.

Hi Mary! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

I am interested in the full list of 455 companies in the data set. Would you please send this to me? Thank you.

Hi Larry! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Thanks for this valuable information!

When did you take this analysis? and on what year(s) the sales took place?

Also, can you provide a link to your next article with the full list?

Thanks Eli! It was written in March 2019. I am working on updating this dataset and analysis this week since A LOT happened this year. I’ve signed you up to be notified of when this post goes live with the full data set.

Thanks, much appreciated

Hi Eli, here it is! Multiples have been updated for post-covid and this time, you can download the full data set here: https://microcap.co/2020software

Please send me the data set, will appreciate it

Hi Rakesh, it should be in your inbox now!